2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  Buy the Dip: Gold Holds Strong at $3980, Targets $4150

Buy the Dip: Gold Holds Strong at $3980, Targets $4150  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

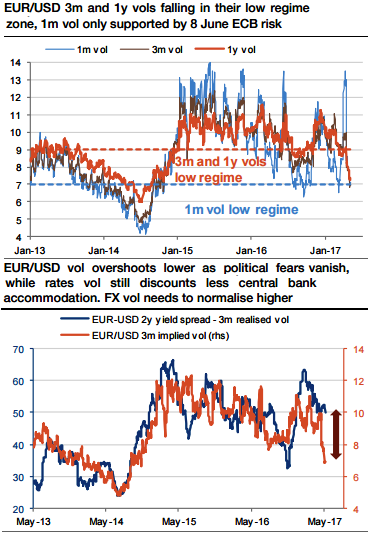

The EURUSD vols have been belligerently sold off in the aftermath of the French presidential election. The markets hailed the election of Macron, shielding a very pro-European programme. The majority of the risk was factored in at the front end of the curve, and the 1m implied returned to lows not seen since 2015 (refer above charts), which marks the start of the current vol regime.

Nonetheless, the longer EURUSD expiries like 3m and 1y vols fell significantly below their lows. This seems intriguing as volatility moves tend to be larger at the front-end. But the 1m vol did not break its lows because it is now pricing the next 8 June ECB meeting.

The last time the low vol regime lasted a certain amount of time coincided with a period when central bank policies were more accommodative than today. This depressed the volatility of short rates, which is powerfully driving FX volatility (refer above charts).

However, we now observe a correlation break between FX and rates volatility, with EURUSD vol under pressure while rates vol remains supported. In our view, relative rates volatility currently better captures the central bank stances than EURUSD volatility.

Lastly, FX vol has been extremely focused on short-term political risk, and its valuation diverged from the medium fundamental background. As the market is now freed from political fears and refocuses on the modalities of ECB tightening, the case for more euro bullishness and more volatility resurfaces.

Thus, we advocated buying EURUSD topside volatility - EURUSD vol sold off aggressively after Frexit fears receded. - The market will now focus on the ECB's 8 June meeting. FX vol has disconnected from rates vol, which has been less impacted by political risk but still resiliently discounts ECB risk.

We recommend going long an EURUSD 1y volatility swap, paying-off volatility realized above 1.05. This condition discounts the entry level via the negative skew. The currency swaps are for exchanging an amount of real cash in one currency for the same amount in another.

EURUSD vol sold off aggressively to its low regime area as political fears vanished.

Is it heading towards a softer regime, or is it a great opportunity to load longs?

The market would now be cautious in the ECB’s stance that is scheduled on 8th June.

However, FX vol disconnected from rates vol, which has been less impacted by political risk, but still resiliently discounts ECB risk.