AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns

Eurozone Recession Risks Rise as Middle East Conflict Threatens Growth, ECB Official Warns  Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

Pound recovers on ‘hawkish’ Bank of England, it is quite easy to cook up story like this. Is it wise enough to give all credits BoE? Well, in FX market, it is not the isolated news that drives the action, we would rather look at in a heterogamous perspective.

No doubt, the pound has experienced an acceleration in its uptrend against the US dollar, but in the recent weeks itself which was prior to the BoE event.

But not disregarding the central bank’s event risk, OTC markets have priced in this news in 1w-1m tenors. Please be noted that the significant shift in risk reversal to positive side as rallies hit the new year-to-date high above 1.3650 at one stage. This was led by a re-pricing of expectations of UK Bank Rate, following ‘hawkish’ minutes from September’s Bank of England (BoE) policy meeting and upbeat comments from Monetary Policy Committee (MPC) members, which caught the market off-guard.

With Brexit negotiations dragging on, we still see downside risks for the pound.

Only once the future relationship between the UK and the EU starts to gain shape do we see room for a sustained recovery of GBP exchange rates.

Even with uncertainty over Brexit negotiations ongoing, the pound gained in September. This was due to the Bank of England (BoE) signaling a rate hike on the back of increasing (core) inflation.

Initially, however, we only see scope for one rate hike, which is unlikely to be sufficient to send the pound higher on a sustainable basis.

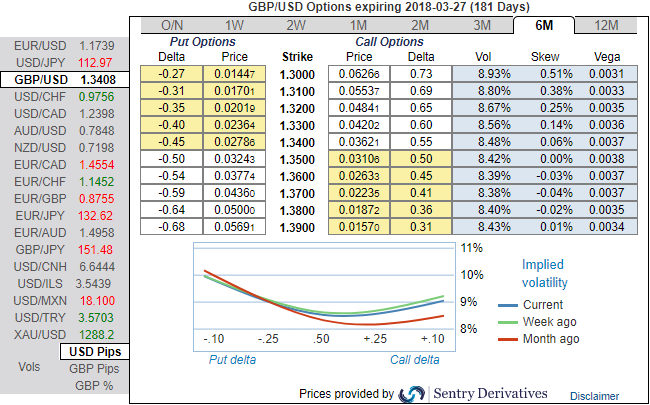

Therefore, the downside risks to the pound will predominate for now. Both the ECB and the Fed are likely to tighten monetary policy before year-end, which is why the pound looks set to lose both against the EUR and the USD. This is also evident if you look into the positively skewed implied volatility of GBPUSD of 6-months tenors that is indicating hedgers' interests in downside risks upto 1.30 levels.

Finally, on the flip side, any cyclical/Fed repricing needs to be considered in context of what is happening in the rest of-world where in some places the recent or potential repricing might be more significant. For example, as mentioned earlier, the more significant policy repricing in the past two weeks was in the UK, and the resulting 3% rise in GBPUSD certainly was a drag on the magnitude the USD index was able to rise on its own policy repricing, and explains why the DXY index (where GBP has a 12% weight) failed to advance in the past two weeks in spite of the Fed story.