Menu

Menu

Search

Search

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Fundamental Evaluation Series: GBP/USD vs. yield divergence review

Jun 27, 2017 09:26 am UTC| Commentary

The chart above shows, how the relationship between GBP/USD and 2-year yield divergence has unfolded since 2012. The cozy relationship between the yield spread and the exchange rate, in this case, is quite visible. Back...

Fundamental Evaluation Series: Yield spread vs. EUR/USD

Jun 27, 2017 07:36 am UTC| Commentary

The chart above shows, how the relationship between EUR/USD and 2-year yield divergence has unfolded since 2012. It is evident that these short rates have been a key influencing factor for the pair as policy divergence...

Fundamental Evaluation Series: Long-term yield spread vs. EUR/GBP

May 12, 2017 09:31 am UTC| Commentary

This chart shows the performance of EUR/GBP exchange rate in contrast to the performance of long-term yield divergence between 10-year German bund and 10-year UK gilt. During our evaluation period beginning August...

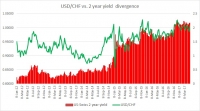

Fundamental Evaluation Series: USD/CHF vs. yield divergence

May 12, 2017 08:48 am UTC| Commentary

During our evaluation period beginning 2012, the yield spread between the US 2-year bond and a Swiss equivalent has widened by almost 200 basis points but the exchange rate hasnt followed through as much as it should have...

Fundamental Evaluation Series: USD/JPY vs. yield divergence

May 12, 2017 08:40 am UTC| Commentary

This one pair has been at odds with yield divergence throughout 2016 as the yen benefited from risk aversion and due to market participants doubts on BoJs abilities to ease policies further. It had shown excellent...

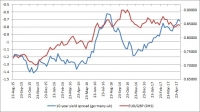

Fundamental Evaluation Series: Yield spread vs. GBP/USD

May 12, 2017 08:29 am UTC| Commentary

The chart above shows, how the relationship between GBP/USD and 2-year yield divergence has unfolded since 2012. The cozy relationship between the yield spread and the exchange rate, in this case, is quite visible....

Fundamental Evaluation Series: Yield spread vs. EUR/USD

May 12, 2017 05:57 am UTC| Commentary

The chart above shows, how the relationship between EUR/USD and 2 year yield divergence has unfolded since 2012. It is evident that these short rates have been a key influencing factor for the pair as policy divergence...

Gold Price Today: Gold Slips as Dollar Rebounds Ahead of Fed Minutes

Dollar Rebounds as Euro, Pound Slip Ahead of Fed Minutes, Yen Near Intervention Zone

Oil Prices Slip as OPEC+ Boosts August Output, Oversupply Concerns Weigh on Crude Market

US Stock Futures Rise as Investors Eye Fed Minutes, AI Stocks, and Q2 Earnings

Gold Price Rises as Softer Dollar and Fed Rate Expectations Boost Bullion Demand

China Submarine Missile Test Sparks Concern Across Asia-Pacific

UN Rights Council Launches Sudan Probe Over RSF Violence in al-Obeid

Russia Strikes Kyiv as Ukraine Faces Patriot Missile Shortage Before NATO Summit

Sara Duterte Impeachment Trial Opens, Putting 2028 Philippine Election in Focus

Flavio Bolsonaro Urges Trump to Delay Brazil Tariffs Until After 2026 Election

Blue Origin New Glenn Explosion Could Delay Launch Operations Until 2028

Blue Origin New Glenn Rocket Explodes During Launch Pad Test, Delaying Space Ambitions

SpaceX Delays Starship V3 Launch Ahead of Potential Record IPO

Trump Administration Releases New UFO Files and Apollo Mission Records

China vs. NASA: The New Moon Race and What's at Stake by 2030

Bank of America Upgrades T-Mobile to Buy, Says LEO Satellite Fears Are Overdone

Foxconn Q2 Revenue Surges Nearly 40% on Strong AI Server Demand

Citi Raises TSMC Price Target as AI Chip Demand Strengthens Growth Outlook

AI Memory Chip Shortage Likely to Persist Despite Korea Investment Boom, Nomura Says

Samsung Q2 Profit Seen Soaring as AI Memory Demand Keeps Chip Prices Elevated

- Market Data