Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

The Reserve Bank of Australia (RBA) left the official cash rate on hold at 1.50% as widely expected. Indeed, the RBA’s commentary today was remarkably similar to its statement in August. Market participants however, were looking for more cautious commentary, as suggested in a spike in the Australian dollar after the release. This comes with a backdrop of increasing uncertainty over the outlook, particularly for the global economy.

RBA Governor Lowe gives remarks later this evening at the RBA Board Dinner which typically involves a reflective and broad ranging speech.

Apparently, AUDUSD shows some sort of consolidation around 0.7200 ahead of the RBA decision this afternoon. A notable change, however was the recognition that the Australian dollar had “depreciated against the US dollar along with most other currencies”.

AUDUSD 1-3 month: The Aussie’s mid-August slide to 0.72 on Turkey-inspired global risk aversion left it quite oversold when judged by our short-term fair value estimate, which remains near 0.75. AU-US yield differentials have continued to drift in the US dollar’s favour in recent weeks but Australia’s key commodity prices have been mixed, overall a little higher since mid-August and a long way above March lows.

Still, AUD risks probably remain to the downside in September (0.70 handle), given the confluence of FOMC meeting, US review of China tariffs and EUR/Italy budget risks. By year-end we see AUDUSD back to 0.73.

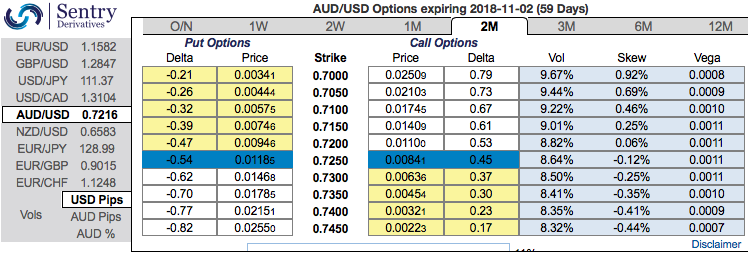

OTC outlook: Most importantly, please be noted that the positively skewed IVs of 2m tenors signify the hedgers’ interests to bid OTM put strikes upto 0.70 levels (above nutshell). While bearish delta risk reversal also substantiates that the hedging activities for the downside risks remain intact.

Currency Strength Index: FxWirePro's hourly AUD spot index is inching towards 34 levels (which is bullish), while hourly USD spot index was at 75 (bullish) while articulating (at 06:43 GMT). For more details on the index, please refer below weblink: