Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

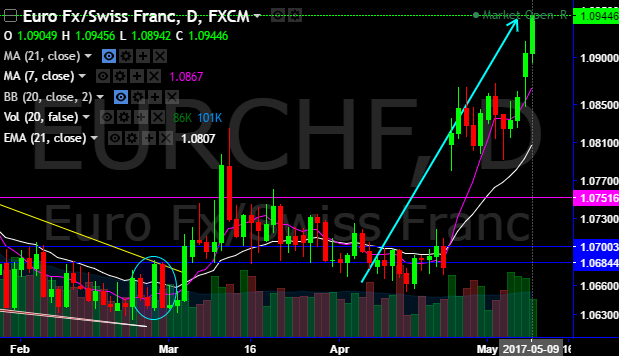

The victory of moderate candidate Emmanuel Macron in the French presidential election has allowed the Swiss franc to depreciate significantly against the euro. This reduces the SNB’s need to intervene. While we still believe the CHF will generally remain under appreciation pressure, levels around 1.09 in EURCHF should be sustained for the time being. However, we expect falling exchange rates again by the end of the year at the latest. The Swiss franc has suffered substantial losses versus the euro since the presidential election in France (refer above chart).

The Swiss National Bank (SNB) should be overjoyed: At EURCHF levels well above 1.08, there is no longer any reason for it to intervene in the FX market to prevent a stronger franc. We, as renowned CHF bulls, also believe current EURCHF levels should actually be sustained. In the short term, there are two factors supporting higher EURCHF levels: (1) the ECB’s monetary policy and (2) brighter risk sentiment with regard to the stability of the eurozone. However, both factors are likely to turn again by the end of the year at the latest.

Options Strategic framework (Long CHF - call spread versus USD; hold vs EUR in spot):

The sell-off in USDCHF was too little, too late for our put spread that expired OTM. We continue to hold a short position in EURCHF as we do not believe that the French election will be a game-changer for EURCHF insofar as it will do little to resolve the powerful balance of payments disequilibrium in favor of CHF. That being said, we are close to our stop and would step aside for a period should this be triggered.

We await Monday's sight deposit data to gauge whether or not the SNB has continued to intervene even in the face of a stronger EUR. As an aside, we find it interesting that the SNB appeared to actively sell EUR FX reserves in 1Q in favor of USD and JPY, thereby undermining the objective of its intervention assuming this is to stabilize EURCHF (SNB probably sold EUR in 1Q17).

In all we are comfortable with the existing cash position in EURCHF, albeit the strikes on the USDCHF have proved frustratingly elusive as expiry looms next week.

Hold a 2m 1.0010 - 0.95 USDCHF debit put spread.

Stay short EURCHF in cash although you have seen sharp spikes that seem momentary, we are expecting the considerable pullback from bearish rallies. Marked at -1.23%.