BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  USA at 250: the Black American struggle for life, liberty and the pursuit of happiness

USA at 250: the Black American struggle for life, liberty and the pursuit of happiness  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

With continued USD weakens, USDCNY dipped to the 6.75 level this morning, i.e. back to the level seen in October. The PBoC set the USDCNY fixing rate at 6.7451, the lowest in nine months. Chinese authorities are again in control of their currency.

On the one hand, capital outflows have been easing due to administrative measures, and China has increased its holdings of US Treasuries for the fourth consecutive month, according to recent TIS data.

On the other hand, the market has gradually turned around their expectations and believes that the CNY weakness, if there is any, will be moderate. Of course, the market only has a very short memory, which means that it could easily forget what it had believed in the past.

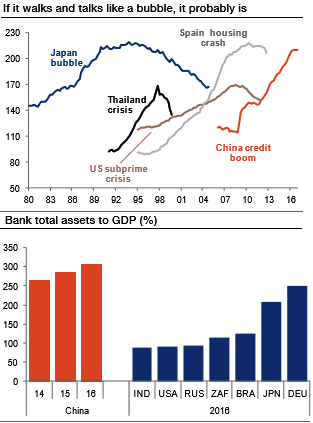

China is a source of angst for global investors with non-financial corporate debt at 166% of GDP compared with 97% a decade ago (refer above chart).

The bursting of a debt bubble in China would have far-reaching negative implications for emerging markets either via the risk sentiment channel or through commodity prices, global growth, and the global supply chain.

History tells us that credit booms lead to bubbles and to eventual crises. In China’s case, the risks are compounded by the large size of the banking system relative to GDP (refer above chart).

It is unclear if, or when, the bubble will burst in China, but it is the major medium-term risk factor for the entire EM currency complex.