Gold Price Rises as Investors Weigh U.S.-Iran Talks and Fed Policy Outlook

Gold Price Rises as Investors Weigh U.S.-Iran Talks and Fed Policy Outlook  Oil Prices Drop as U.S.-Iran Talks Ease Supply Concerns

Oil Prices Drop as U.S.-Iran Talks Ease Supply Concerns  Oil Prices Fall as Iran Peace Talks Progress, Hormuz Reopens, and U.S. SPR Hits 1983 Low

Oil Prices Fall as Iran Peace Talks Progress, Hormuz Reopens, and U.S. SPR Hits 1983 Low  Australia Inflation Cools in May, But Core CPI Keeps RBA Rate Hike Risks Alive

Australia Inflation Cools in May, But Core CPI Keeps RBA Rate Hike Risks Alive  Dollar Holds Firm as U.S.-Iran Talks Ease Tensions, GBP/USD Slips Amid UK Political Uncertainty

Dollar Holds Firm as U.S.-Iran Talks Ease Tensions, GBP/USD Slips Amid UK Political Uncertainty  Asian Stocks Slide as AI Rally Pauses, South Korean Chipmakers Lead Regional Decline

Asian Stocks Slide as AI Rally Pauses, South Korean Chipmakers Lead Regional Decline  Wall Street Slides as AI Stocks Tumble Following South Korea Tech Sell-Off

Wall Street Slides as AI Stocks Tumble Following South Korea Tech Sell-Off  Japan Manufacturing Growth Accelerates in June as Orders Surge Despite Iran War Cost Pressures

Japan Manufacturing Growth Accelerates in June as Orders Surge Despite Iran War Cost Pressures  Asian Stocks Slip as Oil Rebounds Amid Fed Rate Hike Fears

Asian Stocks Slip as Oil Rebounds Amid Fed Rate Hike Fears  Japan, U.S. Discuss Yen Weakness as Currency Intervention Concerns Grow

Japan, U.S. Discuss Yen Weakness as Currency Intervention Concerns Grow  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Gold Prices Mixed as Stronger Dollar Offsets Safe-Haven Demand Amid U.S.-Iran Peace Talks

Gold Prices Mixed as Stronger Dollar Offsets Safe-Haven Demand Amid U.S.-Iran Peace Talks  South Korea Remains MSCI Emerging Market Despite Reform Progress

South Korea Remains MSCI Emerging Market Despite Reform Progress  Russian Stocks End Flat as MOEX Index Hits New 52-Week Low

Russian Stocks End Flat as MOEX Index Hits New 52-Week Low  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  South Korea’s KOSPI Rebounds as Samsung and SK Hynix Lead Tech Stock Recovery

South Korea’s KOSPI Rebounds as Samsung and SK Hynix Lead Tech Stock Recovery  France Faces Long Road to Economic Rebalancing as Weak Demand and High Rates Weigh, Says Citi

France Faces Long Road to Economic Rebalancing as Weak Demand and High Rates Weigh, Says Citi

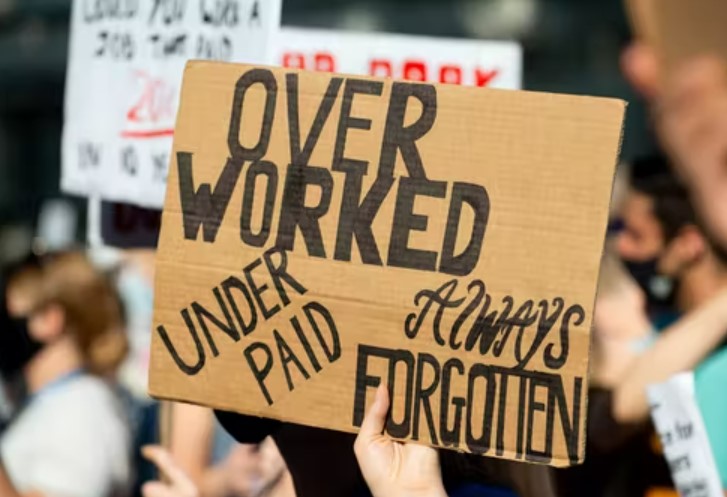

The recent sharp rises in inflation have effectively put an end to three decades of relative price stability in the UK. The prices of most goods and services have gone up and could go even higher.

The reasons for this include increased economic activity after the ending of COVID restrictions, global supply chain issues and the war in Ukraine. And one immediate effect of such steep inflationary pressure is that people’s wages are suddenly not worth as much as they used to be.

In the UK, there have been strikes in 2022 by rail workers and criminal barristers, and warnings of industrial action in sectors such as nursing, education and transport – all seeking pay rises in response to the increasing cost of living.

But while inflation has indeed led to a substantial squeeze on living standards and depressed real wages, there have also been arguments made that increases in wages could lead to further inflation. The so-called “wage-inflation spiral” suggests that wage increases lead to higher price inflation which in turn makes workers demand higher wages.

The basic idea is that the consistent ratcheting up of workers’ pay to match inflation and cost of living increases leads to firms raising prices to protect their profit margins.

Some then, including the governor of the Bank of England, and the former chairman of Goldman Sachs, have called on both employers and employees to exercise “wage restraint”.

These interventions are easily (and often) criticised on the grounds that a person earning close to £500,000 a year (as the governor does) is not best placed to tell millions of people who earn much much less that they should settle for what they’ve got. But even if we ignore this moral dimension, there are still major flaws in the argument for not increasing wages.

Firstly, the notion that wage increases lead directly to an increase in inflation does not always hold. The current high inflation rate is largely caused by factors which are not connected to pay levels, so will not be solved by restraining wages. Secondly, a restriction on real wages is likely to bring forward the prospect of a recession.

The UK (along with the US and many European countries) is already showing a decline in economic growth. Allowing wages to fall in real terms is only likely to make this situation worse by squeezing household incomes. This squeeze will inevitably lead to a decrease in consumption and spending, putting further pressure on the economy. It is also likely to push many more people into poverty. The negative effects of wage restraint cannot be ignored.

Wage watch

It is also worth looking ahead. The most recent forecast by the Bank of England suggests that by the middle of 2025 there are risks of “deflation” – a reduction in general price levels across the economy. And while some may welcome the idea of price falls, deflation brings its own serious risks, including higher unemployment and lower economic growth.

What is needed now is urgent action to ensure that wages rise in line with inflation, so consumption and spending is maintained to avoid or at least dampen the expected recession. This will require workers to bargain for pay rises, and employers to provide them.

Improving morale. Shutterstock/Tony Stock

And yes, it will also probably mean more strikes in the public sector – but the government needs to come to terms with the economic value of raising public sector pay. Public sector workers – after years of pay freezes – deserve a pay rise. Their colleagues in the private sector also need and merit an uplift in their wages.

Finally, progress in pay and the move to a sustainable recovery will require a state determined to raise productivity. Increases in wages will themselves create the conditions for higher productivity by boosting the motivation and morale of workers. Higher wages can support the economy and help to avert the threat of stagnation – and ward off even higher inflation, and an even greater cost of living crisis.

David Spencer has received funding from the ESRC.

David Spencer has received funding from the ESRC.

Muhammad Ali Nasir does not work for, consult, own shares in or receive funding from any company or organisation that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.