AI Memory Boom Sparks Global Chip Supply Crunch

AI Memory Boom Sparks Global Chip Supply Crunch  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game

World Cup technology: from ref cams to AI analysts, cutting-edge research is changing the game  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill

The recent slide in the US dollar has continued with the greenback dropping by around 4% against the euro so far in July alone to around 1.17. The move against the pound has been less pronounced but has seen GBPUSD move up above 1.28 despite ongoing Brexit negotiations weighing on sentiment. Of late, in the US, Fed policymakers have been very vocal about their worries that the economic recovery could falter with the rise in Covid-19. Last week’s reported increase in US jobless claims won’t alleviate those worries.

Market sentiment, risk of a US 2nd wave and US election have all concurred in driving the US Dollar down over the past 6-weeks or so. EUR remained supported yesterday as ECB kept rates and its emergency monetary stimulus unchanged. As the dollar dropped more than 6% on a trade-weighted basis from end of March highs, there has been interest from market participants in obtaining some correlation-discount when selling the Dollar. The cross-asset strategy team maintains a bullish stance on markets, given cheapness of Equities over bonds, policy support and rebound in growth, unlikely to be put at risk by new lockdowns.

In the FX vol space, the picture above is consistent with the steady decline of vol levels since late March, and with the output of our tactical filter keeping a short-Gamma bias since May, after flashing the most extreme risk-off signals on record throughout March and into April. Yet, low valuations from a historical standpoint and a macro agenda that could trigger vols in the second half of the year made us support a slightly more defensive positioning, favoring RVs over outright short vol (RVs and vol ratio spreads still the game).

In our upcoming posts, we propose directional and long-Theta constructs by investigating the interdependence of smile, vol curves and correlation parameters.

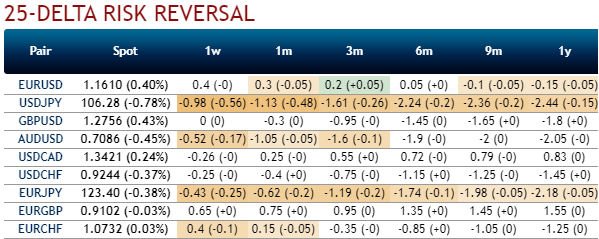

EURUSD risk reversals have still been indicating the hedging sentiments for the bearish risks in the long run, as the fresh negative bids are added to the positive RRs for 1-3m tenors (1st chart).

Most importantly, the positively skewed EURUSD IVs of 3m tenors are stretched on either side but with slight biasness towards downside hedging risks (refer 2nd chart), while IVs are shrunk below 6.75% across major tenors. Courtesy: JPM