UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns

Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance

BOJ Rate Decision in Focus as Yen, Inflation, and Nikkei Hang in Balance

Usually, there would always be a build-up before major events. Likewise, ECB seems to be limiting the tractability: ECB President Draghi hinted at the last press conference, that the central bank had by in no manner casted-off all its missiles yet.

In its monthly report, it sees upside risks for the economy thanks to strong exports and good prospects for industrial production, which strengthens the reasons for reducing the monthly ECB purchases. Even if ECB President Mario Draghi does not want to announce these in Jackson Hole – he will not be able to distance himself notably from them either. After all the legal limits self-imposed by the ECB are getting increasingly close.

That means Draghi’s appearance will be a balancing act - not just as far as ECB policy is concerned but also as regards the euro. The euro too was mentioned in the Bundesbank’s monthly report. Price pressure from abroad is likely to ease as import prices have already fallen recently due to the strong appreciation of the euro. Even if Draghi does not even want to suggest a verbal intervention against EUR strength he cannot come across as completely carefree regarding the euro either.

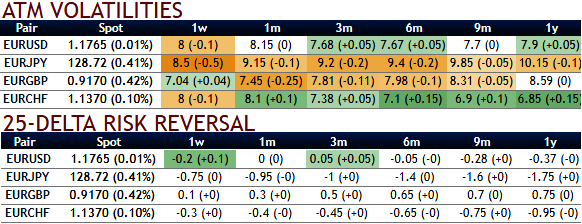

Consequently, the influential beta-forces of euro-strength/dollar weakness continue to preserve prevailing vol themes of gamma strength, vol curve flattening and risk-reversal underperformance.

Event premium over a busy late August-September period spanning Jackson Hole and ECB/Fed meetings is relatively underpriced in GBP and SGD. USDCHF 3M3M FVAs have lagged the recent upturn in CHF complex vols and are value buys along a mildly inverted curve.

Please be noted that the implied vols of euro crosses have been tepid despite the series data flows are lined up.

Today’s data announcements:

France Markit Mfg, Service and composite Flash PMIs, Denmark Consumer Confidence, Germany Markit Mfg, service and composite PMIs, Eurozone Markit Mfg, service and composite Flash PMIs.

EUR vol risk reversals remain low compared to the level of rates. Also, in longer tails, the EUR volatility smile remains flat compared with the rates vs vol correlation seen since 2015 and over the past week.

FxWirePro launches Absolute Return Managed Program. For more details, visit: