Bank of England Set to Hold Interest Rates as Inflation Risks and Iran War Impact Loom

Bank of England Set to Hold Interest Rates as Inflation Risks and Iran War Impact Loom  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing

Bank of Japan's Ueda Flags Low Real Interest Rates as Key Factor in Rate Hike Timing  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty  AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Although the Yen appears under pressure momentarily as BoJ caps nominal yields and risk sentiment holds up, but the move in relative real yields between Japan and the US represents a clear case for a weaker yen. The risk is for risk sentiment to change, thus the resilience of the risk mood bears watching because it is the key to the yen's continued weakness.

It has fallen by over 7% against the dollar since the election, more than any other Asian currency. A steady move higher in US yields is not expected to trigger a durable deterioration in risk sentiment for a while.

In addition, the BoJ’s strategy of capping nominal yields is paying dividends, as any pickup in domestic inflation expectations drives Japanese real yields down. The USDJPY, therefore, has scope to rally considerably further. We look for the USDJPY to reach 120 by September.

The dollar is unlikely to strengthen due to a flight-to-quality but would be boosted by higher US long yields being lifted by a sharp repricing of US inflation expectations.

Shorting the costly vols to trade a gradual move uncertainty is not going to lift volatility until the environment turns risk-off. So far, the Trump victory has not triggered such a shift. On top of that, the USDJPY uptrend is likely to slow down after the initial topside acceleration in autumn 2016.

As the suspicion, the Japanese central bank’s yield control transferred rates volatility towards FX volatility. But yen depreciation should now be more gradual. The recent fast upside lifted the 6m implied volatility to its highest level since 2014.

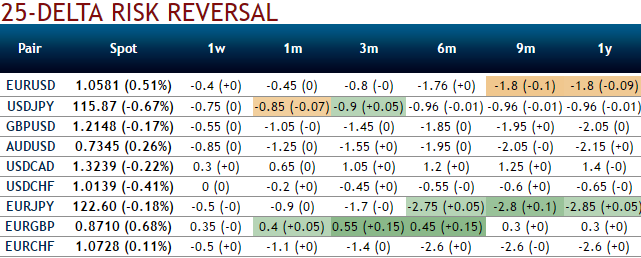

USDJPY 1m risk reversals and 2m IV skews are evidencing mounting hedging interests for downside risks (while articulating).

While the 2m realized volatility peaked at 18, it is already retracing much lower. With no risk-off shift in sight, and vega volatility still having to adjust to short-term dynamics, a short volatility structure makes sense.

Accordingly, a trade on “buy right-and-hold tight” logic is designed so as to match volatility regimes. It states the volatility but should suffer from initial negative convexity.