AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says

AI-Driven Inflation Raises U.S. Consumer Prices, Goldman Sachs Says  Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns

Goldman Sachs Delays Fed Rate Cut Forecast to 2026 Amid Rising Inflation Concerns

Recent price action at the long end has also prompted many market participants to raise concerns about a sharp selloff as China reduces its Treasury holdings. We believe the impact on long-term rates is unlikely to be significant for a few reasons.

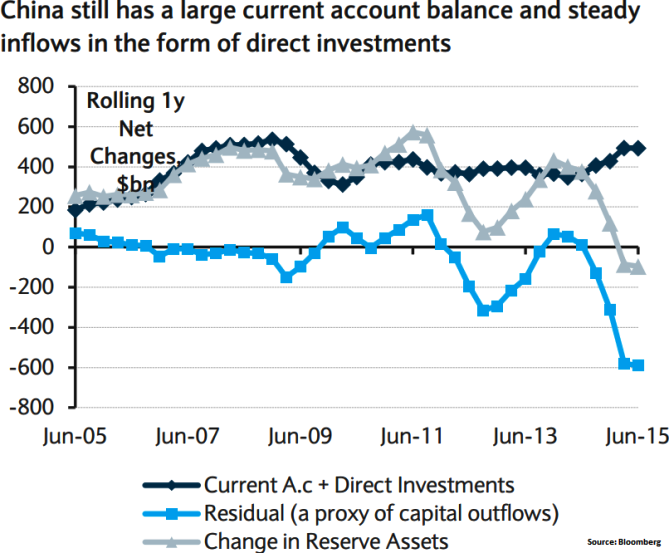

First, China is still running a large current account balance and continues to see steady inflows related to direct investments. Figure shows that over the past year (ending June 15) the two have accounted for roughly $490bn in inflows (Current Account = $290bn + Direct Investments = $200bn). With the currency weakening, the trade balance is likely to grow (even if it stays unchanged as a share of GDP, it should still grow in absolute terms). Hence, China can withstand significant amount of capital outflows, before having to significantly reduce its FX reserves, in our view. Note while reported FX reserves declined roughly $300bn between June 14 and June 15, the actual decline in reserves was only $96bn; the rest was due to currency adjustments. In fact in Q2 15, reserves rose $13bn.

Second, while in recent days, there may very well have been a reduction in China's Treasury holdings, we believe that should not have had much of an effect on long rates. Since the distribution of China's holdings is not reported, we use this as a proxy. The average maturity in mid-2014 was four years with 75% of holdings less than five years and this maturity profile has remained stable, suggesting a desire by official investors to keep the portfolio relatively in the front end. Hence, any reduction should not have been a major duration supply event. In fact, China's (+Belgium's) Treasury holdings have been already been declining since the middle of last year without much of an effect, in our view.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Chinese monetary policy measures may disrupt treasury holdings

Friday, August 28, 2015 11:58 AM UTC

Editor's Picks

- Market Data

Most Popular