Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Oil Prices Drop as Middle East Supply Recovery Eases Market Concerns

Oil Prices Drop as Middle East Supply Recovery Eases Market Concerns  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Asian Markets Rally as Micron and Qualcomm AI Outlook Lifts Global Tech Stocks

Asian Markets Rally as Micron and Qualcomm AI Outlook Lifts Global Tech Stocks  Gold Drops Below $4,000 as Strong US Dollar and Fed Rate Hike Expectations Pressure Bullion

Gold Drops Below $4,000 as Strong US Dollar and Fed Rate Hike Expectations Pressure Bullion  S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges

S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges  Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand

Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand  Trump Threatens 100% Tariffs on Countries Imposing Digital Services Taxes on U.S. Tech Firms

Trump Threatens 100% Tariffs on Countries Imposing Digital Services Taxes on U.S. Tech Firms  South Korea’s KOSPI Jumps Over 5% as Samsung, SK Hynix Rally on Micron Earnings Boost

South Korea’s KOSPI Jumps Over 5% as Samsung, SK Hynix Rally on Micron Earnings Boost  White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response

White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

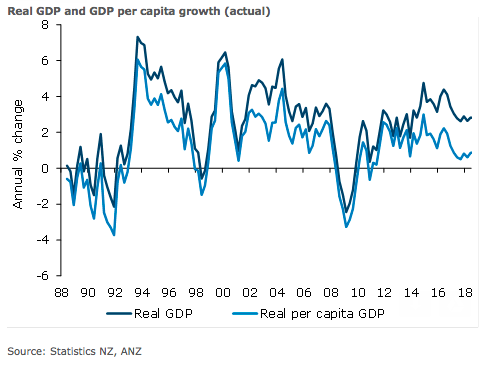

The New Zealand economy is expected to have expanded 0.5 percent q/q in Q3, reflecting a touch of payback from Q2’s strong 1.0 percent q/q print, but with the deceleration limited by stable underlying momentum, according to the latest report from ANZ Research.

This would see annual growth moderate to 2.7 percent in Q3 from 2.8 percent, within recent ranges and consistent with expectations that growth will remain range bound at 2-1/2-3 percent over the next couple of years.

The seasonally adjusted current account deficit is expected to narrow in the quarter, but widen in annual terms to 3.6 percent of GDP on base effects.

More broadly, migration-led population growth has been flattering headline growth this entire cycle, contributing around two thirds of the economic expansion in recent years. And while this is set to provide a boost for a while yet, easing net inflows imply a shrinking impetus to growth going forward.

A 0.6 percent q/q rise in services industries is expected to make the largest contribution to quarterly growth: 0.4 percentage point, led by wholesale trade (up 1.2 percent q/q) and arts and recreation (up 3.0 percent q/q).

"Broadly speaking, we suspect ongoing strength in population growth will continue to make its presence known on the services side, with small quarterly gains across most components. In fact, the only source of significant weakness among the services components is expected to come from accommodation, which appears set to retrace Q2’s solid rise," the report commented.

Goods production is next on the list, and expected to rise 0.6 percent q/q, making a 0.1 percentage point contribution to quarterly growth. A 1.0 percent q/q lift in construction is at the fore here, while both food (up 0.1 percent q/q) and ex-food manufacturing (up 0.3 percent q/q) look set to record modest rises.

Meanwhile, the seasonally adjusted Balance of Payments deficit is expected to narrow around USD0.4 billion from Q2, driven by a narrowing goods deficit as growth in exports outpaces that of imports. The 0.3 percent fall in the Q3 OTI terms of trade suggests this will be entirely volume driven.

The services surplus is expected to narrow a touch as seasonally adjusted exports partially retrace some of Q2’s strength and imports lift. The income deficit is expected to widen, with primary income outflows lifting on the back of growing international debt and equity liabilities. The annual current account deficit is expected to widen 0.3 percentage point of GDP to 3.6 percent, owing to base effects, ANZ Research added in its report.