FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX

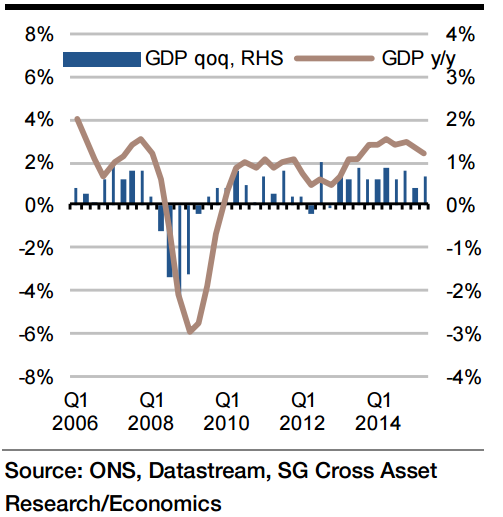

The first estimate of Q3 growth will be the usual output estimate. The news from the high frequency data is that industrial production will make a very modest positive contribution to growth but that construction will be a drag of nearly 0.2pp. The latest construction output data showed output plunging by over 4% mom in August and if it just holds at that level in September would be down 2.6% on the quarter.

As usual, the crucial factor will be the service sector. The services PMI points to a marked loss of momentum in the sector as the third quarter progressed so growth in services output is expected to have no more than matched the Q2 performance of 0.6% qoq, although the strong Q3 retail sales performance brings a small risk of an increase.

This implies that GDP growth should fall from 0.7% qoq in Q2 to 0.5% in Q3.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

UK GDP growth slowing in Q3

Monday, October 26, 2015 8:30 PM UTC

Editor's Picks

- Market Data

Most Popular