US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

BOJ Minutes Signal More Rate Hikes as Inflation Risks Grow

The U.S. currency has surged since the election, partly in anticipation of fiscal policies under the incoming Trump administration. The Bloomberg Dollar Spot Index, which measures the greenback against 10 global currencies, had appreciated 5.2 pct between Nov. 8 and the end of FOMC’s meeting on Dec. 14. Since then it has strengthened an additional 1.1 pct.

A stronger dollar hurts growth by making U.S. exports less competitive and slows inflation by making imports cheaper.

The trade gap in the United States increased to $42.6 billion in October of 2016, up $6.4 billion from a downwardly revised $36.2 billion in September. Exports recorded the biggest decline since January due to lower shipments of food, industrial supplies and materials, automobiles, consumer goods and soybeans while imports reached the highest in 14 months.

At their December meeting, officials raised the number of quarter-point rate hikes they foresee in 2017, to three from two, while signaling growing confidence in the economy, according to their median estimate.

FED’s forward guidance – Signs of three hikes out of seven schedules in 2017 stimulates 6m-1y USD OTC hedging functions:

Universally known fact, Fed rate has not been an exception, which is likely to rise more than once in 2017 which in turn, yields on US treasuries are surging higher. Also, the US Fed has stepped up monetary policy tightening and had signaled for more tightening in next few policy meet in 2017. This, in turn, is also creating sufficient ground for inflation to rise (target rate 2%).

Notably, the prospects of expansionary fiscal policy in the US under Trump regime that likely drives US interest rates higher and therefore strengthen the dollar further. Trump is also likely to protect US manufacturing in order to generate more and more employment and this could actually narrow US trade deficit.

The Trump presidency would run until 2021 which will be among most inflationary in last few decades and the market has already started discounting it.

Trump may put a break on long-term interest rates and convince Fed not only to refrain from further interest rates hikes but also to launch another round of long-term treasury debt purchases in case the economy loses momentum, another round of quantitative easing. Further, his proposals to increase spending and cut taxes will fuel economic growth in 2017 and will thus, also prompt Fed to raise interest rates.

The probability of 50-75 bps rate hike during the first half of 2017 while 25-50 bps in the latter half of 2017 is higher according to the current reading of CME Group’s FedWatch tool. This indicates that there is a high level of confidence in the market about the Fed decision to hike interest rate in 2017.

OTC updates:

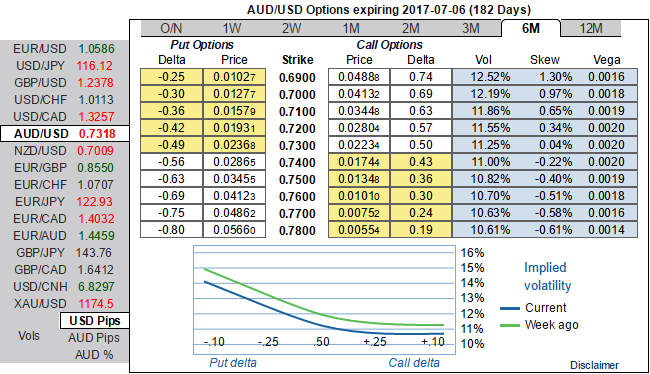

Please be noted that the risk reversals of dollar crosses are considerably signaling bullish risks in longer tenors in the dollar. As shown in the diagram positively skews in AUDUSD shows the hedgers interests in OTM puts, as a result, we could expect more bearish risks in this pair, same is the case in EURUSD, while USDCAD has been bullish as the positively skewed IVs signal OTM call are on more demand comparatively. You could probably understand by now, the impact of Fed’s hints of more hawkish approach in its monetary policy in upcoming meetings.