European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

The major event in this week’s UK economic calendar is the BoE’s MPC meeting that is scheduled on this Thursday. Whilethe political and economic backdrop remains momentarily constructive of sterling’s underperformance. Nevertheless, we continue to be short, using near-term upswings by unwinding the GBPUSD expression of the trade since this is currently in the money but has only less than a week to expiry and is close to the strike.

There is very little intrigue this time – having raised Bank Rate to 0.75% at the start of last month, policy makers will refrain from making further changes to current policy or their forward guidance.

The recent economic data have been broadly consistent with the BoE’s updated economic projections published last month – although July’s CPI was a touch below its forecast – and so they will maintain their expectation that further policy tightening over the forecast horizon will be required in order to return inflation sustainably to the 2% target.

Perhaps the most interesting detail about the meeting is that it will be the first one attended by newly appointed external member Jonathan Heskel, Professor of Economics at Imperial College London, who has replaced the hawkish Ian McCafferty on the MPC.

Looking at GBP against a UK data surprise index, the British currency has not paid much attention to the improvement in UK data since June, weighed by other factors including Brexit. As such, any rally in response to strong data is likely to be relatively short-lived, with the resumption of Brexit discussions on Thursday to guide sentiment.

Yes, among G10 FX universe, the attention of the likelihood of a ‘no deal’ issue is keeping Brexit risks front and centre, and has taken a toll on the pound remarkably: GBPUSD has shed 2.2% MTD after the near 3% decline since early June, GBPUSD 1Y ATM vol has risen, gained 1.2vol pt since July and 1Y 25D risk-reversals have broadened to levels last seen early last year. We discuss hedging breaks below.

While the loudness of ‘no deal’ Brexit likelihood has intensified in the recent past, following International Trade Secretary Liam Fox’s pegging the odds of such a scenario at 60% in an interview. It is reckoned that the consequences of a no deal outcome are too fraught for it to be a serious policy consideration, however, continued media coverage of the issue is keeping Brexit risks front and centre of investors’ radar.

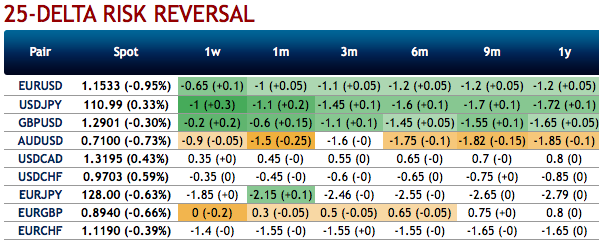

Before we proceed further, let’s just quickly glance through the hedging outlook in FX OTC markets and formulate strategies.

Please be informed that the positively skewed IVs of 6m tenors signify the hedgers’ interests to bid OTM put strikes upto 1.20 levels.

While the positive shift in delta risk reversal numbers (across 1-3m tenors) indicates mild recovery is anticipated in the underlying movements amid the bearish hedging activities for the downside risks remains intact in a medium-term perspective.

One could argue that GBP vols and risk-reversals have not kept pace with the trend increase in political risks in the UK since the Brexit referendum. Considering 1.20 on GBPUSD to be the hard Brexit threshold – not unreasonable since 1.20 is the spot low in the aftermath of the Leave vote in 2016 – pricing on 1Y 1.20 strike GBP put/USD call digital options of 15.7% of USD notional (mid) at current market (1.2776 spot reference) strikes us as being on the low side, on net indicating that option markets assign more than 50% additional probability to a benign resolution to UK/EU. Courtesy: JPM

Currency Strength Index: FxWirePro's hourly GBP spot index is inching towards 142 levels (which is bullish), while hourly USD spot index was at -52 (bearish) while articulating (at 08:28 GMT). For more details on the index, please refer below weblink: