Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

What is happening to the euro? All eyes are currently on the US dollar, and as a result, the single currency is taking a bit of a back seat, despite the fact that the ECB meeting is taking place next week. As is usually the case in the run-up to meetings, there is little in the way of comments by ECB officials. At least the recent comments did not result in anything unusual (the hawks hawkish, ECB President Draghi rather cautious as far as the sustainability of the rise in inflation is concerned) which the market would have to translate into a major euro move. Even though the US President continues to provide material creating movement in USD as did his Treasury Secretary Steve Mnuchin by announcing yesterday that Trump’s twitter feed about depreciation had been a “warning shot” for China and Russia.

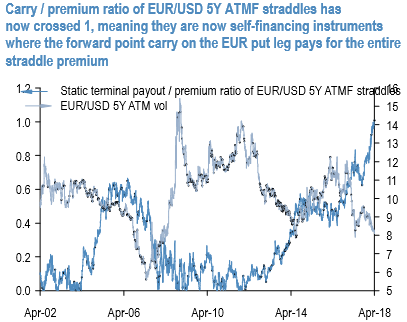

It is commented earlier on the discrepancy between broadening forward points in EUR-and EUR-crosses and relatively tame levels of vol in comparison, a combination that has resulted in an explosion in carry-to-vol ratios in these pairs.

In short, positive static carry at expiry (assuming spot remains unchanged) on the EUR put the leg of ATMF EUR straddles is sizeable enough to cover a good fraction of their premium, meaning vol ownership has become a lot less onerous from a decay standpoint than before.

This carry-to-premium ratio for EURUSD 5Y straddles crossed above the never-before-experienced threshold of 1 for the pair last week, meaning that 5Y Euro vol is now a self-financing financing asset (refer 1st chart).

Absolute vol levels are also low in a historical sense (below the 10th percentile of available history); the combination of depressed vols and high carry/vol ratios has historically been a good set-up for strategic vol ownership, especially in EM currencies.

Additionally, some of the same arguments that we made with respect to the cheapness of 5Y Yen vol apply to Euro – namely that 5Y ATM has fallen more than 1 vol and the 5Y –1Y vol slope has flattened 0.7 pts. (i.e. 5Y vol has declined more than 1Y) even when EURUSD 5Y forwards (YTD + 4.7%) have outpaced spot (YTD +2.3%) due to the well-documented decoupling between FX and rate differentials this year.

The difference with yen is that the mispricing of EURUSD 5Y vol relative to short-dated FX vol and the EUR and US swaption volatilities is not as extreme as in 2008 (refer 2nd chart) as is the case with USDJPY. In an ideal world, another 1-vol of additional misalignment would set-up excellent entry levels into outright vega longs.

In short, buying EURUSD vol with a directionally bullish Euro baseline is somewhat unexciting and lacks a bit of enthusiasm as a standalone alpha bet. Valuations are positive, however, hence there is a place for long-end EUR vega within an overall portfolio hedging context. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: