Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

At the start of the FOMC meeting the US central bankers are experiencing strong headwinds for their rate hike plans. This time round mainly from the US President who took another swing at the Fed yesterday. It was “incredible” that it was “even considering” hiking interest rates further. Of course, he was backed by his closest advisors. According to his trade advisor, Peter Navarro, the Fed should act in a more data dependent manner. And the argument that the Fed had to hike interest rates to prove its independence would as well be unjustified.

First of all: if the administration did not attack the Fed’s approach in such an open manner the Fed would not be in the situation in the first place where it has to defend its independence.

Secondly: yes, a rate hike to demonstrate its independence is exactly the right step in this situation. The resilience and stability of a currency depends directly on the strength of the institutions that back it. The best negative example this year was Turkey.

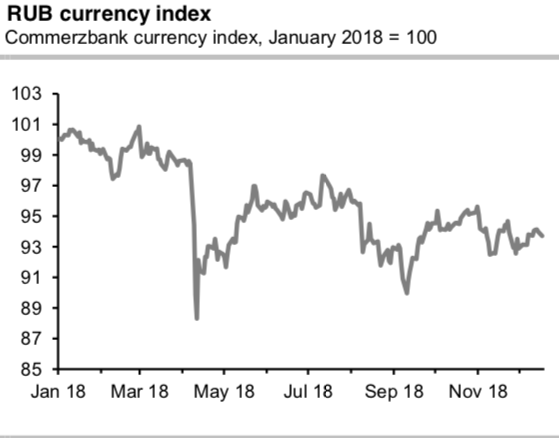

The best positive example: Russia. Shortly after the Russian Premier voiced his support for lower interest rates the Russian central bank hiked key rates in a surprise move. It surprised the market again with another rate hike just a while ago. By doing so, the bank leaves no doubt what its priorities are.

As a result, the Russian currency has stood up impressively well this year (Refer above chart) – despite geopolitical tensions, Emerging Market turbulence and a continued weak economy.

Resumption of FX purchases will prove bearish for RUB, in our view. The CBR announced resumption of FX purchases from January 15th. This is likely to weigh meaningfully on RUB, in our view. The currency has struggled to appreciate while purchases were suspended and the full current account surplus was allowed to support the FX market. With FX purchases in place, the current account support will be much smaller.

Meanwhile, recurring geopolitical tensions are likely to weigh on capital flows. Notably, the central bank now indicated that any future RUB weakness is much less likely to be met with renewed suspension of the program. This, in our view, both increases the scope for depreciation in RUB as well as the chances CBR will deliver more hikes.

Trade recommendations:

RUB: We maintain our 11-January-2019 1x1 USDRUB (68/71) call spread. We may have been a bit early with this trade as the resumption of purchases was now announced only for January 15th, after the expiry of our option. Yet, amid global EM risks and negative RUB seasonality around the year-end, we still see a good chance RUB will weaken in anticipation of the budget rule headwind within the remaining maturity of the trade.

TRY: At spot reference: 5.3393 levels, contemplating above driving factors, on hedging grounds we would like to uphold RV trades - 3m USDTRY put up-and-in Short 1m put.

Currency Strength Index: FxWirePro's hourly USD spot index is flashing at -77 levels (which is bearish), while articulating at (12:53 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex