Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

The much-awaited ECB QE recalibration exercise ultimately announced yesterday, but it contained very few surprises after a meticulous 6w build-up and ended in a virtual stalemate for FX and rates markets, with EUR crosses fluctuating lower but within recent ranges and the rates complex flattening fractionally at the long end. If it ever was the objective to dash speculation of a rate increase before 2019, the ECB succeeded with verve.

On forward guidance, the ECB made clear that interest rates will stay at their present levels for an extended period of time, well past the horizon of the “net” asset purchases.

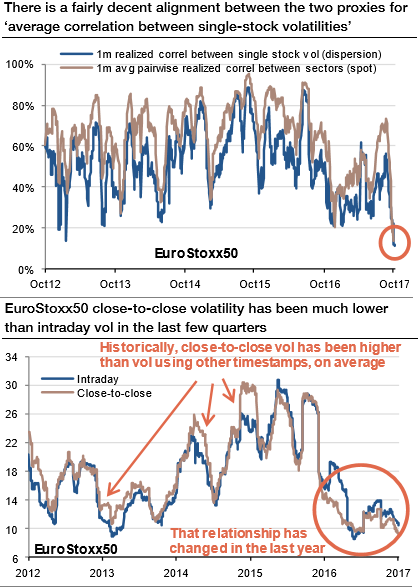

Volatility across all indices in Europe has continued to sink slowly as if pulled down in a quagmire. That may be a fitting analogy because volatility has been sticky and on a downward trend through the year. The 1-month realized volatilities on the CAC40, DAX30 and SMI indices have reached their lowest levels since the inception of these indices, while the volatilities on EuroStoxx50, SMI and AEX are close to all-time lows. Long vol positions have been painful to carry for a while, and unfortunately, investors may be looking at more of the same for a while.

To simplify and approximate in a Black Scholes model, gamma is inversely proportional to volatility and gamma of options increases when volatility decreases (Refer above chart). This is understandable as gamma is defined as the change in the delta of the option for 1% move in the spot and the second order sensitivities are going to be larger for a 1% move in an environment which is currently experiencing c.30bp moves a day (5% realized vol). Nevertheless, it is worth looking at the charts below to visualize the scale of the increase in gamma and what it means for subsequent hedging from dealers.

As seen in the chart below, gamma becomes much more concentrated around the ATM in a low vol environment, leading to a 4x times increase in gamma sensitivity as vol decreases from 20% to 5%.

Our largest net position is long EUR against USD, GBP, and CHF. The ECB taper announcement is expected to be marginally constructive for EUR, the European central bank hasn’t delivered fireworks as expected.

Option pricing of the October ECB event risk is a tad expensive since the outcome of a slower-for-longer QE extension, and given the recent history of consistent under-delivery in EUR-crosses on ECB meeting dates. The post-ECB rolldown in short-dated EURUSD implied vols is overstated, and there is much better value in owning 1M forward volatility after the event.