US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns

BOJ Holds Interest Rates at 0.75% as Policymakers Signal Growing Inflation Concerns  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

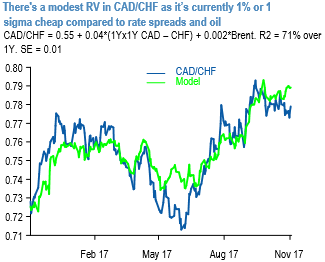

The BoC was the first central bank to pivot in a more dovish direction in the summer. But after delivering its second successive rate hike in October and signaling a greater data dependency, rate expectations have corrected somewhat. The recent labor data should provide some renewed impetus to the tightening cycle as wage growth moved up to 2.4% oya compared to 0.7% only six months ago.

Admittedly the CAD curve discounts two hikes next year but thereafter it is pretty flat, so there’s scope for the longer-dated term premium to increase on evidence that labor slack is not as great as the BoC believes.

While the SNB maintains its view that the CHF is "highly valued", as the situation remains "fragile". The expectation continued vigilance from policymakers even as EURCHF 1.20 looms.

We pair CAD vs CHF because:

1) We want to avoid an outright USD short,

2) We are not comfortable adding to existing JPY shorts given the possibility of trade tensions during Trump’s Asian tour, and

3) The demand for Swiss franc funding is likely to persist in a more reflationary global environment in which the SNB is content to sit on its hands. Swiss CPI is released on Monday – this is already at a 6-year high and above the 20Y average, but optically it is hard to get excited about inflation that is still below 1%. There is a modest RV edge to CADCHF as the cross is around 1%, or 1-sigma, cheap on a high-frequency model (refer above chart). Courtesy: JPM