Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics

Bank of England left its monetary policy unchanged but the dissenting votes for an immediate 25bps hike, from the current Bank Rate of 0.50%, rose from two to three (Chief Economist Haldane, who has broken ranks verbally before, joined known hawks McCafferty and Saunders). In addition, due to the generally lower levels of rates, the Bank lowered the rate at which they would consider altering their asset holdings to 1.5% (from 2.0%). That remains a distant prospect given that their outlined path of three 25bps rises is over the next three years. The statement and minutes confirmed their prior view that the economy was recovering as projected and that 1Q weakness was temporary.

Over 2018, we see scope for some further underperformance from NZD, as we expect ongoing confirmation that the RBNZ can credibly lag policy normalization in the G3. Evidence that real assets (equities, housing) are threatened by late cycle growth dynamics and government intervention would add further weight to this story. NZDUSD is expected to depreciate to 0.66 by 2Q’19.

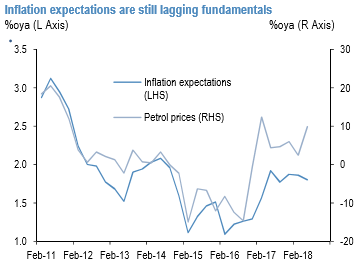

RBNZ Governor Orr’s first MPS maintained the low for long policy guidance, with an evenly balanced outlook for the near-term. The Governor stated the next move is equally likely to be up or down and has placed significant weight on the fact that inflation expectations have become more backward-looking, which slows the recovery from several years of below-target outcomes. Such headwinds were highlighted in the most recent RBNZ expectations survey, where 1Y forward expectations remain lower than would be expected, in the context of rising oil prices (refer 1st chart).

NZD faces domestic headwinds to local rates that are only now being fully appreciated. Growth has weakened, the central bank’s inflation forecasts have been revised materially lower, net immigration is slowing and business confidence has fallen significantly since the change of government.

While the Aussie has been one of the worst performers in the broad-based US dollar rally since the June FOMC and ECB meetings. But the RBA should also be optimistic on Australia’s growth outlook in its Aug statement. Courtesy: JPM & Westpac

Currency Strength Index: FxWirePro's hourly NZD spot index is inching towards -26 levels (bearish), while hourly USD spot index was at -110 (bearish), GBP flashes at 139 (bullish) and AUD at 35 (bullish) while articulating at 07:32 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit: