Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy

Mary Daly Says AI Uncertainty Clouds Fed Rate Outlook Despite Restrictive Policy  Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027

Taiwan Central Bank Likely to Keep Interest Rates Unchanged Through 2027  Smartphones are helping filmmakers tell the stories the movie industry overlooks

Smartphones are helping filmmakers tell the stories the movie industry overlooks  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  South Korea Warns Won Is Undervalued, Boosts FX Coordination With Japan

South Korea Warns Won Is Undervalued, Boosts FX Coordination With Japan  Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target

Morgan Stanley Names BAE Systems Top European Defence Stock Despite Lower Price Target  Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns

Oil Prices Slip as Iran Talks and Strong Supply Outlook Ease Market Concerns  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations

Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro

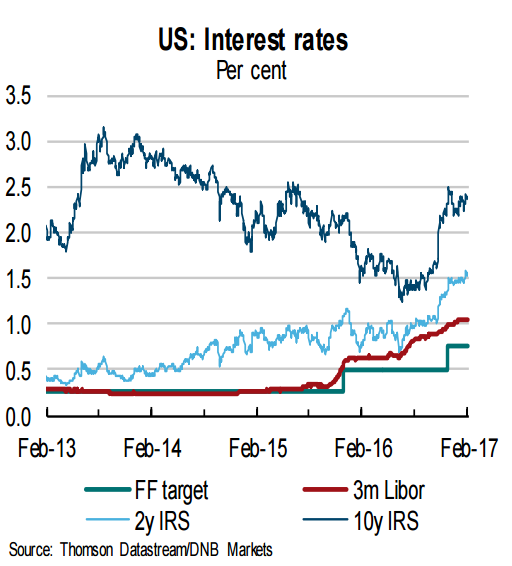

Minutes of the Federal Reserve's Jan. 31-Feb monetary policy meeting published earlier this week on Wednesday showed that many policymakers believed another interest rate hike might be appropriate "fairly soon" if labor market and inflation data meet or beat expectations. Most members expect a continuation of moderate expansion in economic activity and a gradual rise in inflation to target over the medium-term.

Data released on Thursday showed that U.S. initial jobless claims for the week ending February 18 rose slightly last week by 6,000 to a seasonally adjusted 244,000. It was the 103rd straight week that claims remained below 300,000, a threshold associated with a healthy labor market. The four-week moving average in initial claims, considered a better gauge, fell modestly, to 241,000 from 245,000, in a sign of a strengthening labor market.

"Altogether, we see little in the recent jobless claims data to change our view on labor markets. Despite some volatility in the data around year-end, the claims data continue to point to a low rate of separation activity in labor markets and are suggestive of favorable labor market conditions overall." said Barclays capital in a report.

The next payrolls report will clearly be key, but we also have a stream of speeches from Fed speakers between now and the 16 March decision which will be important for shaping expectations. Furthermore, the core PCE inflation release for January, due 1. March will also be important. Fading optimism surrounding US President Donald Trump's proposed fiscal policies dimmed prospects of a Fed rate hike move at its upcoming meeting in March.

"We maintain our call for two hikes in 2017 - most likely in June and December," said Knut A. Magnussen, Senior Economist DNB Markets.

Markets were looking for a firmer signal from FOMC minutes and were left disappointed after the release. The USD sold off and bonds rallied post the release on Wednesday. Thursday's comments from Treasury Secretary Steven Mnuchin, providing little details for the proposed tax reforms, did little to ease market concerns. Broad-based US Dollar selling extends on third consecutive session. USD/JPY was trading at 112.33, while EUR/USD was at 1.0607 at 1200 GMT.

FxWirePro's USD hourly strength index was bearish at -70.1237. For more details on FxWirePro's Currency Strength Index, visit http://www.fxwirepro.com/currencyindex.