South Africa Eyes ECB Repo Lines as Inflation Eases and Rate Cuts Loom

South Africa Eyes ECB Repo Lines as Inflation Eases and Rate Cuts Loom  Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic

Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic  MAS Holds Monetary Policy Steady as Strong Growth Raises Inflation Risks

MAS Holds Monetary Policy Steady as Strong Growth Raises Inflation Risks  RBA Expected to Raise Interest Rates by 25 Basis Points in February, ANZ Forecast Says

RBA Expected to Raise Interest Rates by 25 Basis Points in February, ANZ Forecast Says  Bank of Japan Signals Readiness for Near-Term Rate Hike as Inflation Nears Target

Bank of Japan Signals Readiness for Near-Term Rate Hike as Inflation Nears Target  ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence

ECB’s Cipollone Backs Digital Euro as Europe Pushes for Payment System Independence

Following the attempted coup and the wave of purges by the Erdogan government, the Turkish economy slipped into recession. But according to official data, GDP jumped in Q4 by a hefty 3.9% in the quarter.

Monthly data releases paint a different picture. Falling tourism revenue, a widening trade deficit, a surge in the unemployment rate – this is not consistent with the GDP release.

Yet, it seems we have to base our forecast on official data. We see GDP growing at a rate of 3.3% this year.

On the back of the lira weakness, inflation rose to 11.3% in March, and the core rate came in at 9.5%. The real interest rate is thus still around zero. Inflation pressure should remain high this year.

A softer dollar, falling bond yields in developed markets and funding costs that are kept at relatively high levels in Turkey have stabilized the lira. Should this continue the central bank will likely start to lower average funding costs gradually. This should exert pressure on the TRY.

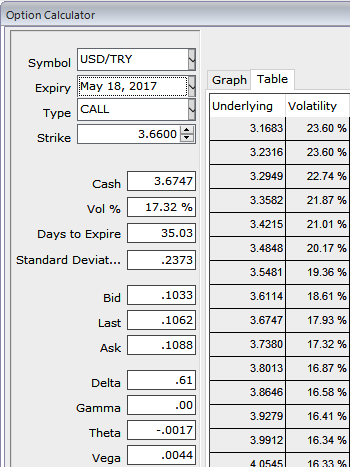

Hedging Framework:

At spot reference: 3.6750, capitalizing on prevailing dips of this pair one can load up shorts in ITM calls and longs in either ATM or OTM calls in a credit call spread with a narrowed strikes of similar expiries.

While the major uptrend could be arrested by the longs of the underlying pair with longer tenors as the 1m ATM IVs are spiking above 17.32%.

So it is advisable to initiate Credit Call Spread (DCCS) in order to tackle both short-term dips and major uptrend.