Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert

Japan Signals Surprise Yen Intervention Strategy as BOJ Hawkish Stance Puts FX Traders on Alert  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro

We structured a bearish AUDJPY view through a calendar spread of one-touches (short a 3m one-touch put, long a 6m) to capture the good-bad duality in Trump's policy platform. The markets have been squarely focused since the election on a pro-risk loosening in fiscal policy and corporate deregulation, but the positive impact on risk sentiment and cyclical crosses such as AUDJPY could yet be reversed should the new Administration deliver on its protectionist agenda and vacillate over fiscal reform.

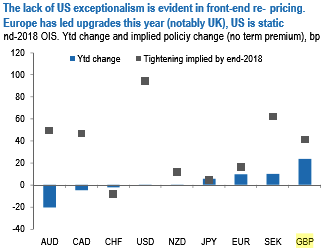

Aside from the broader risk backdrop, monetary policy developments have been modestly negative for AUDJPY insofar as AUD rate expectations have been under more negative pressure this year than any other G10 country (refer above chart).

This week's Q4 CPI data confirmed the disinflationary price dynamics that are a challenge to the RBA (trimmed mean inflation hit a new record low of 1.6%) even allowing for the new governor’s switch in emphasis from inflation to financial stability.

We continue to expect two more cuts from the RBA this year, albeit we have pushed back the first of these from February to May, around the expiry of this trade.

Short 3m/long 6m AUDJPY 78.0 one-touch puts in 0.69:1 notional for net premium 31.0%.