South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations

Alcohol is one of the most dangerous drugs, yet its presence is ubiquitous in social settings and celebrations  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’

State of emergency in Crimea as Ukraine focuses pressure on ‘jewel in Putin’s crown’  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

The medium-term view on the euro remains bullish in anticipation of a pivot in ECB policy. EURJPY year-end forecast is between 129.50 and 130.50 and likely to persist to be in the little-extended range during Q1 majorly owing to two significant factors.

Firstly, Italian and Japanese elections’ risks to dominate.

Secondly, in the October meeting, we now expect the ECB to announce a slower but longer taper, specifically a 9month QE extension at €20bn per month versus our earlier expectation of a 6-month extension.

Recent political developments in the Euro area have garnered attention. In Spain, the acrimonious standoff between the central and Catalan government has intensified uncertainty following the illegal referendum in which 90% of the voters voted for independence, resulted in a 20bp widening in Spain-Germany yield spreads intra-month.

Historical experience from valuation frameworks suggests that euro valuations are not yet a constraint for further strengthening. On long-term valuation metrics, even though the euro has strengthened by 15% in TWI terms since the post-QE bottom, historical experience from other major currencies where markets perceived an impending end of QE programs showed a larger, 26% strengthening in TWI on average.

Chart 3 shows that dollar rallied by as much as 27% from its post-QE bottom, GBP rallied by 22% as markets priced in a less accommodative policy from the BoE (till the prospect of Brexit halted/ reversed that march higher) and JPY strengthened by 30% post QE2 as markets doubted the inability of the BoJ to deliver any additional QE (yield curve control was not being discussed at that time).

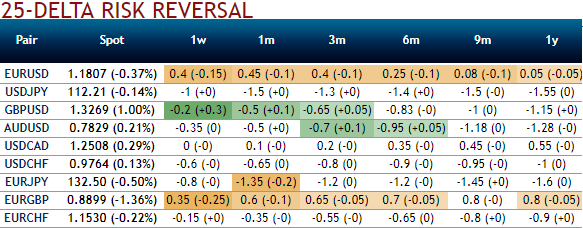

Please be noted that the risk reversals are still indicating bearish risks, while positively skewed IVs of the same tenor signifies the hedgers’ interests in OTM put strikes. On the flip side, if you look at the technical chart of this pair, the major trend has been rising higher. The technical indicators have also been substantiating the strength and momentum in this consolidation phase.

Hence, we advocate diagonal credit call spreads on hedging grounds to participate both short-term downswings and long-term upswings.

This option strategy to keep the potential bullish price risk caused out of fundamental events on the check.

Keeping the both fundamental and technical factors in mind, it is advisable to initiate long in 3M (1%) OTM 0.36 delta call while writing 1m (1%) ITM call with positive theta and delta closer to zero (both sides use European style options), this credit call spread option trading strategy is recommended when the underlying spot FX price is anticipated to drop moderately in the near term and spikes up in long term.

The return is limited by ITM shorts. No matter how far the market moves below that point, the profit would be the maximum to the extent of initial premiums received.