UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why

Despite its best efforts, Iran won’t be able to toll the Strait of Hormuz. Here’s why  Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit

Goldman Sachs Says China Competition Weighs More on EU Growth Than Trade Deficit  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Economic pessimism has set in – but there are reasons for Australians to be hopeful

Economic pessimism has set in – but there are reasons for Australians to be hopeful  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

ECB Keeps July Rate Options Open Amid Iran War Energy Price Risks

The recent developments in the Swiss franc have been less intense over the past month than in the latter part of July when the surge in EURCHF fuelled an expectation in certain quarters that the franc was on the cusp of a material downgrade against a resurgent euro.

SNB is scheduled for its Libor rate announcement today which would be out shortly and streets’ consensuses are that SNB to maintain status quo.

You can foresee bearish scenarios of CHF given the fact that SNB resumes FX intervention at higher spot rates than previously and can be bullish if SNB desists from intervention over a multi-month period. Potential trigger events are SNB intervention (weekly sight depos, monthly stats, P&L on Swiss reserves)

The key interrogation over franc valuation: Notwithstanding the SNB's repeated assertions that the franc is “significantly overvalued", there is the little economic impact from said overvaluation. The Swiss current account, for example, is the largest among the G10 economies, and it has averaged over 10% of GDP in the past few years despite the franc's sharp appreciation. Even on the question of the franc’s valuation, one could derive vastly different conclusions using either the PPP or FEER methodologies (refer above chart).

Gradual reflation: The climbing Swiss PMI indicator and the cyclical upswing in the euro area suggest that Swiss growth should be well supported in the coming quarters, despite the recent weakness in the GDP data. CPI inflation readings have also been trending fitfully higher into positive territory since late 2015, albeit still languishing under 1%. Switzerland, therefore, appears to fit well within the broader European reflation story.

Broad euro strength lifting EURCHF: The SNB fought hard to staunch franc appreciation in the past few years, and EURCHF has finally started to climb as the ECB inched toward policy normalization. The Swiss franc remains a favorite safe haven currency, but barring global volatility spikes, we expect EURCHF to be dragged gradually higher by the appreciating euro. (Refer above graph).

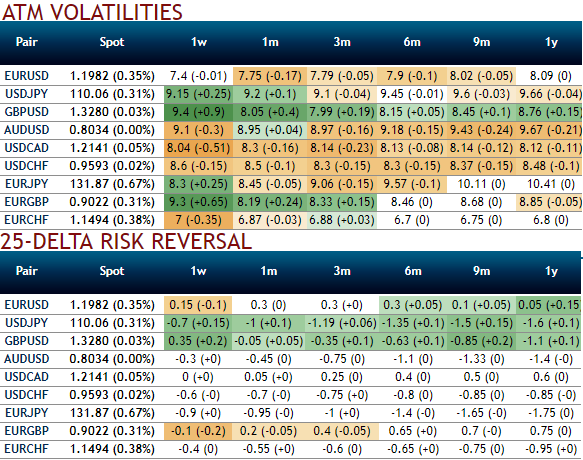

SNB needs to lag the ECB: The ambiguity regarding the franc’s valuation means that the SNB cannot rely on a valuation mean-reversion process. It remains the key that the SNB continues to lag the ECB in policy normalization. Weaker inflation in Switzerland certainly argues for greater prudence on the part of the SNB. The CHF vols and correlations have soared following the recent spike in EURCHF, but IVs have still been tepid (least among the FX pool) and JP Morgan reckons that the flipside of this, lack of participation is the availability of RV opportunities in the CHFCHF-cross option space.

Currency Strength Index: Ahead of Swiss central bank’s monetary policy, FxWirePro's hourly CHF spot index was at shy above -97 (highly bearish) at 06:47 GMT. For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex.

FxWirePro launches Absolute Return Managed Program. For more details, visit:

http://www.fxwirepro.com/invest

Courtesy: JP Morgan, SG