Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty

Japan Inflation Expectations Rise as BOJ Rate Hike Timing Faces Uncertainty  U.S. Stock Futures Hold Steady as Investors Monitor Iran Tensions and Key Economic Events

U.S. Stock Futures Hold Steady as Investors Monitor Iran Tensions and Key Economic Events  Oil Prices Slip Amid Iran Ceasefire Extension, Hormuz Disruptions Keep Markets Tense

Oil Prices Slip Amid Iran Ceasefire Extension, Hormuz Disruptions Keep Markets Tense  Oil Prices Slip as U.S.-Iran Tensions and Ceasefire Uncertainty Weigh on Markets

Oil Prices Slip as U.S.-Iran Tensions and Ceasefire Uncertainty Weigh on Markets  USMCA Talks Set to Resume as Mexico Signals New Round of Trade Negotiations

USMCA Talks Set to Resume as Mexico Signals New Round of Trade Negotiations  Asian Stocks Mixed as Tech Shares Decline While Japan’s Nikkei Hits Record High

Asian Stocks Mixed as Tech Shares Decline While Japan’s Nikkei Hits Record High  Asian Stocks Rise on AI Optimism and Iran Peace Talk Hopes

Asian Stocks Rise on AI Optimism and Iran Peace Talk Hopes  Asian Currencies Stay Range-Bound as Dollar Holds Steady Ahead of Fed Nominee Hearing

Asian Currencies Stay Range-Bound as Dollar Holds Steady Ahead of Fed Nominee Hearing  Carney Warns Canada Must Rethink U.S. Ties Amid Trade Tensions and Sovereignty Concerns

Carney Warns Canada Must Rethink U.S. Ties Amid Trade Tensions and Sovereignty Concerns  Rising Jet Fuel Costs from Iran Conflict Push Airfare Higher Across Europe

Rising Jet Fuel Costs from Iran Conflict Push Airfare Higher Across Europe

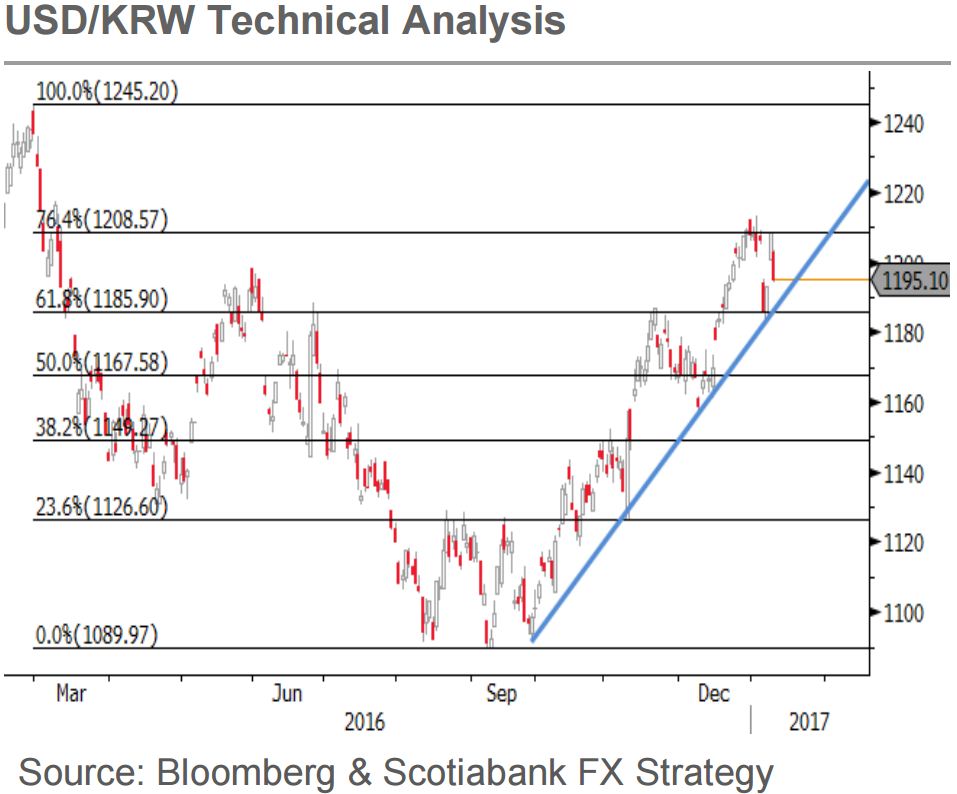

The KRW is likely to lead broad declines in regional currencies amid external uncertainty and domestic turmoil. The ideal strategy is to buy USD/KRW on dips and wait until the pair reaches 1,250 level in the months ahead.

“We also identified a divergence between KOSPI Index and USD/KRW starting 5 December. Continued equity inflows failing to shore up the KRW to a corresponding level have intensified our concerns over the KRW outlook,” said Scotiabank in its research note.

The Bank of Korea (BoK) is expected to hold its first monetary policy meeting on Friday, January 13. It is widely expected to keep its benchmark interest rate unchanged at 1.25 percent for foreseeable future as exports picked up on the back of global demand recovery.

Also, the markets are expecting that the central bank will reduce its number of monetary policy meetings to 8 from previous 12 in 2017. The BoK has been seen avoiding the economic growth slowdown in the last quarter of 2016 amid ongoing political angst in the country as the country’s exports rebounded following the recovery in global consumption.

Moreover, the recovery in energy prices in 2017 boosted inflation expectations for South Korea. This has resulted in a consumer inflation growth, which is holding above 1 percent for four consecutive months as of December 2016, reducing the room for rate cuts.

“Considering all, the best option is still for the BOK to maintain status quo. We expect the repo rate to remain at 1.25 percent by the end of this year,” said DBS Group Research.

It is worth noting that the BoK Governor Lee Ju-yeol has hinted during a New Year speech that the central bank will pay closer attention to financial stability issues when setting monetary policy in 2017. Given this, we do not expect any interest rate change from the BoK in the near future.

On the contrary, the central bank will not be pressurised from the recent appreciation in KRW, which rose 1.2 percent against USD last week, as the KRW should still be under depreciation pressure against the USD in 2017, in line with Korea’s economic underperformance.

Lastly, rate hikes may help to mitigate capital outflows and support the currency. However, domestic household debt is very high and the corporate sector is undergoing restructuring. Premature rate hikes could induce more stress on the indebted households/companies – unless a significant recovery in wage growth/corporate profits is in sight, DBS reported.