US Yen Intervention Unlikely to Deliver Lasting Recovery, Yardeni Says

US Yen Intervention Unlikely to Deliver Lasting Recovery, Yardeni Says  Oil Prices Set for Steep Weekly Losses as Hormuz Deal Stalls

Oil Prices Set for Steep Weekly Losses as Hormuz Deal Stalls  US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise

US Dollar Gains as Iran Tensions, Fed Rate Hike Bets Rise  China Trade Surplus Beats Forecasts in July as Exports Stay Strong

China Trade Surplus Beats Forecasts in July as Exports Stay Strong  Australia Trade Surplus Returns in June as Iron Ore, Coal and LNG Exports Surge

Australia Trade Surplus Returns in June as Iron Ore, Coal and LNG Exports Surge  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue

Canada, US Hold Constructive Trade Talks as Tariff Negotiations Continue  US Stock Futures Rise as Markets Await July Payrolls Data

US Stock Futures Rise as Markets Await July Payrolls Data  Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises

Asian Stocks Cautious Ahead of US Jobs Data as Oil Rises  China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

China Exports Beat July Forecasts as AI Demand Fuels High-Tech Trade

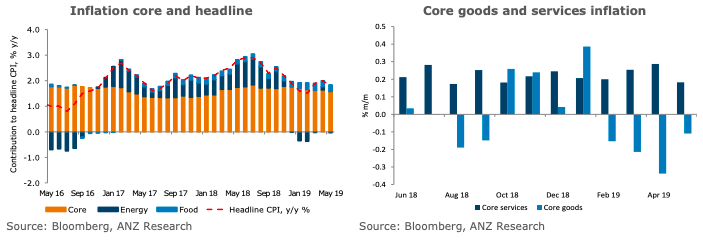

The United States’ core inflation is expected to rise by a 0.2 percent m/m in June after four consecutive months of just 0.1 percent. Underlying pricing pressures remain subdued. Domestic demand could use an extra bump to boost cyclical inflationary pressures, according to the latest report from ANZ Research.

The forecast pick-up in core inflation is predicated on an expected rebound in the prices of goods after contracting for four consecutive months. Both apparel and used vehicle prices should rise after a lengthy period of weakness.

That said, uncertainty surrounds the trajectory of apparel prices following Bureau of Labor Statistics’ (BLS) methodological change earlier this year. The BLS has expanded its sources of data to include outsourcing some of the data collection rather than relying only on its traditional in-house surveys.

Also likely contributing to higher goods prices in June should be the after effects of the US administration’s decision to raise the tariff rate on USD200bn of Chinese imports from 10% to 25% on 10 May.

This would add at most 0.1 ppt in total to the rate of inflation, according to analysis (Inflationary Effects of Trade Disputes with China) from the Federal Reserve Bank of San Francisco. Only a small part of this amount would likely occur in the month of June.

"We look to FOMC Chair Powell’s testimony and the June meeting minutes for guidance on the timing of easing. With the market pricing a 25bp cut in July as a done deal, Fed speakers need to push back if this is unwarranted. A further deterioration in global manufacturing and lackluster domestic inflation suggest that a cut is warranted soon," the report further commented.