Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery

China Keeps Loan Prime Rates Unchanged for 13th Straight Month as Policymakers Prioritize Credit Demand Recovery  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

RBNZ Monetary Policy Statement will be important in setting the tone for 2019. Unlike the Fed, and RBA, which had a hiking bias they could jettison, the RBNZ doesn't really have a tightening bias to unwind. NZD crosses have been weaker, we could foresee NZDUSD at 0.63 levels by H1’2019.

The Governor has already been stating that “the timing and direction of any future OCR move remain data dependent”, and has made little reference to the eventual rate hikes laid out in the staff’s projections. This may make it difficult to match the degree of volte-face executed by other central banks of late, though it seems likely the Governor will try to meet the market by emphasizing global downside risks.

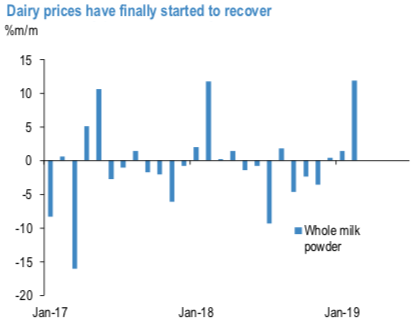

Looking beyond rate differentials, local catalysts for NZD are mixed. This week’s labor market data saw unemployment move back up to 4.3%. However, this comes after 3Q’s stunning drop to a 10-year low, so unemployment is still a touch below where it was six months ago, and probably 1%-pt below NAIRU. Dairy volumes are growing more strongly than they have for some time after prior supply disruptions. Dairy prices have rallied in recent auctions, though posted a similar seasonal pattern last year which was not sustained (refer 1stchart).

In contrast to Australia, where the export-relevant commodity markets are tight, prices are high, and large exporters have seen large profit gains, New Zealand’s exporters are starting any tentative recovery in China demand from a place of weakness (refer 2ndchart). The fall in oil prices will likely offer some reprieve to trade outcomes, but exports are unlikely to benefit from any stabilization in China’s GDP growth that is geared toward fixed asset investment. A shift to stronger consumption outcomes in China would be more positive, however, so the administration’s focus on tax cuts could prove supportive.

The RBNZ (the sole banking regulator in NZ) has slightly extended its consultation period for the Bank Capital Review. The Governor announced in December an effective doubling of tier one capital requirements, well beyond analyst expectations.

Amid all the above aspects, please be noted that FX options hedging activity of this pair is also in sync with the above projections. 6m IV skews have clearly been indicating bearish risks. Hence, major downtrend continuation shouldn’t be panicked the broad-based bearish outlook amid minor rallies.

These positively skewed IVs of 6m tenors signify the hedgers’ interests to bid OTM put strikes up to 0.63 levels (refer above nutshells evidencing IV skews). Courtesy: Sentrix & JPM

Currency Strength Index: FxWirePro's hourly NZD spot index is inching towards 29 levels (which is mildly bullish), while hourly USD spot index was at 27 (mildly bullish) while articulating (at 11:22 GMT).

For more details on the index, please refer below weblink: http://www.fxwirepro.com/currencyindex