BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data

The European Central Bank (ECB) is scheduled for the monetary policy on July 25th. ECB’s readiness to cut its key rate next week. And there is no reason for the euro to appreciate considerably in the short run.

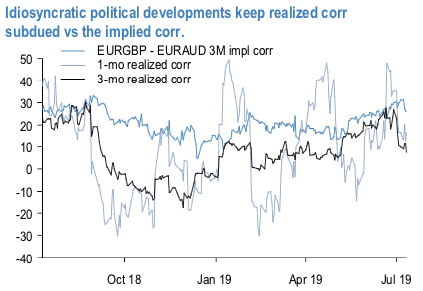

The currency differentiation and short correlation were laid out as one of the core vol alpha themes for H2 in the Mid-Year Outlook. One class of trades that were identified in there was selling GBP vs. commodity FX correlation on the view that GBP’s idiosyncratic political dynamics would lead to low / no correlation with other cyclically sensitive FX.

One such corr short that could be considered at current levels is EURGBP vs EURAUD: 3M implied corr is 26% vs. 2-wk realized corr -4%, 1-mo 16% and 3-mo 7% (refer 1stchart). The backtest in chart 2 shows favorable historical performance over the past 3-yrs since the Brexit vote.

A pushback is that if the ECB pivots towards re-starting QE later this year the EUR could fall against everything in sight and lift all EUR-x vs EUR-y realized correlations, as it happened when EURUSD fell from 1.40 to 1.05 during the ECB QE of 2014-16.

Two ways of guarding against this:

a) The limit expiry to pre-September ECB, when a 10bp rate cut is expected and when a potential QE announcement might come; and/or

b) Hold appropriately sized EURUSD put spreads against a short corr. swap, but sizing is a non-trivial problem.

With 2M EURGBP – EURAUD corr swap @24/35 indic we think vol spread is an attractive alternative to consider: 2M GBPAUD – EURGBP vol spread @0.95/1.45 indicative. Courtesy: JPM