Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions

RBA Raises Interest Rates to 4.35% Amid Rising Inflation Risks and Middle East Tensions  RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200

RBA Rate Hike Outlook: Impact on AUD/USD and ASX 200  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027

OECD Sees Bank of Japan Raising Interest Rates to 2% by 2027  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty

Paraguay Holds Interest Rate at 5.5% as Inflation Remains Stable Amid Global Uncertainty  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

BOJ Governor Kazuo Ueda Hints at Rate Hike as Inflation Pressures Build

The global economy is surfing a cyclical upturn, and financial markets have been gorging on central bank accommodation, but as post-crisis policies are dismantled, the appearance of calm in FX-land risks being deceptive.

The Fed was first out of the blocks with a strong policy response to the global financial crisis, prompting the Brazilian finance minister to bemoan ‘currency wars’. The election of Shinzo Abe as Prime Minister of Japan brought the BoJ into the fray, and by the start of 2015, the ECB had joined in and a significant dollar rally was underway.

As the ECB edges towards normalization, an undervalued euro has room to rise further, and even if the BoJ is committed to its current stance, the yen’s a dormant volcano only in the sense that it hasn’t erupted for a couple of years.

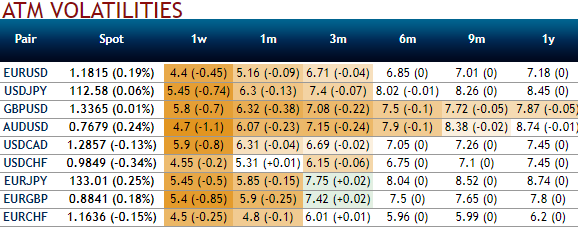

Despite a packed week of central bank meetings and data releases, 2017 the trading year is going out rather quietly into the night as far as FX vol markets are concerned (refer above nutshell showing lackluster ATM IVs). Fireworks of last December are conspicuous by their absence this time around, with any chance of a last hurrah for the dollar in a rather forgettable year dashed by no changes to the FOMC’s plan of three unhurried hikes amid strong, non-inflationary growth in 2018.

VXY has once again collapsed to the lows of the year with Fed risks out of the way and the holiday season in sight and delta-hedged returns over the past 2-weeks across various G10 FX blocs have been in the red with the exceptions of CAD - (oil related whipsaw) and SEK - (post-CPI beat gyrations) crosses (refer above chart).

Of the latter, sharp SEK strength after a strong CPI print is a reasonable template for what might be expected of similar surprises in other currencies next year and is a potential source of thematic alpha for vol investors willing to do the hard yards of event trading with short-dated options. CAD-cross vols are also of interest as a potential buy given NAFTA risks in 2018, and CAD correlations that trade at a substantial discount to trailing realized corrs are well priced as carry friendly trade disruption hedges.

More tactically, option books heading into the year-end could do worse than to own these two recent vol outperformers funded with the bottom two (GBP and USD), since short-horizon relative return momentum of delta-hedged straddles has historically proven to be a reliable factor for volatility risk allocation across currency blocs, outperforming naïve sell-and-hold benchmarks (refer above chart).