U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate

Elon Musk’s Empire: SpaceX, Tesla, and xAI Merger Talks Spark Investor Debate  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data

The 6th round of the NAFTA negotiations comes to an end in Montreal today. While CAD traders had so far paid little attention to the progress of the negotiations this is likely to have changed following the last meeting of the Bank of Canada (BoC).

By now everyone is likely to have realized that the future of NAFTA would not only have an enormous effect on the Canadian economic outlook but that even the continued uncertainty of the matter might affect the BoC’s rate hike path.

An uncertainty that might continue for some time yet - according to a report, industry representatives and people close to the negotiations assume that the negotiations might be extended beyond the current deadline of 31st March maybe even into the next year. In Montreal, no significant progress has been made on any of the critical issues.

We expect more details from the statement at the end of this negotiation round. We assume that CAD will react much more sensitively to NAFTA headlines than it did in the past.

Hence, ahead of uncertainty NAFTA and trade tensions. Accordingly, MXN is anticipated to strengthen to 18.40 with improvement in NAFTA sentiment.

Meanwhile, option pricing suggests a decent build-up of event risk premium in MXN vols: 2W MXN ATM vols @13.4 have rallied to their highest levels since before the start of negotiations last summer, and CAD 2W ATM is 1.5vols above 2017 levels. Current O/N vols are indicating a fairly punchy 1.5-1.7% spot move breakeven for USDMXN and 1.0% for CAD over the Jan 24-26 period.

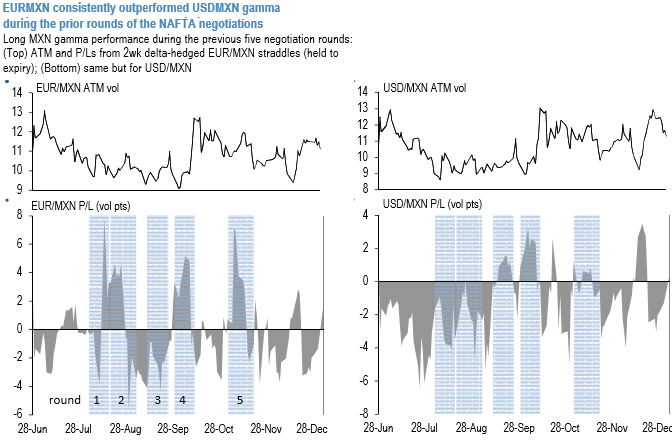

An analysis of MXN gamma performance during the five previous rounds of negotiations (refer above chart) shows that EURMXN tends to consistently outperform USDMXN around these events, perhaps because the more liquid and closely watched USD-vol has tended to attract the bulk of the hedging flows. EURMXN 2w straddles exhibited significant positive returns around two rounds of talks, modest gains in two others and losses during only one round.

While this limited sample analysis indicates a strong positive skew to gamma returns, ex-post event P/Ls have been heavily conditioned on favorable ex-ante vol pricing.