BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead

BOJ Expected to Hold Rates Steady While Signaling More Hikes Ahead  Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist

Chile Central Bank Holds Interest Rate at 4.5% as Inflation and Global Risks Persist  BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook

BOJ Rate Decision in Focus as Sticky Inflation, Weak Yen Shape USD/JPY and Nikkei Outlook  Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields

Japan PM Sanae Takaichi Unveils Growth Plan as BOJ Independence Concerns Lift Bond Yields  China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven

China Holds Loan Prime Rates Steady for 14th Month as Economic Recovery Remains Uneven  Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist

Brazil Cuts Selic Rate to 14% as Inflation Eases but Risks Persist  South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening

South Korea Raises Interest Rates to 2.75% as Inflation and Weak Won Drive Tightening  RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

RBI Holds Repo Rate at 5.25% as Inflation Risks and Global Uncertainty Persist

It was more than obvious that the ECB would extend its QE programme beyond March 2017. As a result it did not seem necessary to mention in great detail that ECB President Mario Draghi indicated just that. It seemed unlikely to me that a sufficiently large number of FX market participants would be taken by surprise by this statement. However, it would seem that this is exactly what happened.

The effects on the banking system and potential adjustments to the ECB programme, there is one key effect on all market participants, which stems from the fact that the market needs to digest two problems:

First, the excess reserves of the banking system as a whole would rise by EUR 80 bn per month. If anybody ponders the banks could prevent this development by lending more, they would need to explain to me why lending has not risen yet. In addition, the ECB reserves are obviously rising by roughly this amount every month – just look at the figures.

Second, it is up to the individual banks to implement the increase in the excess reserves of the banking system as a whole. Good news in euro area is that the German and French PMI prints managed to produce upbeat numbers.

Elsewhere, Last week’s speech from RBA governor Lowe and the minutes from October’s Board meeting added little to Australia’s monetary policy discussion.

RBA minutes deviate little from the rhetoric of the past few meetings due to the following data events.

Australia’s jobless rate down to 5.6%, though survey details continue to print on the softer side.

Q3 CPI the focus next week; headline forecast to print at 0.5% QoQ, while core expected at 0.3% QoQ.

RBA’s monetary policy decision on cash rates.

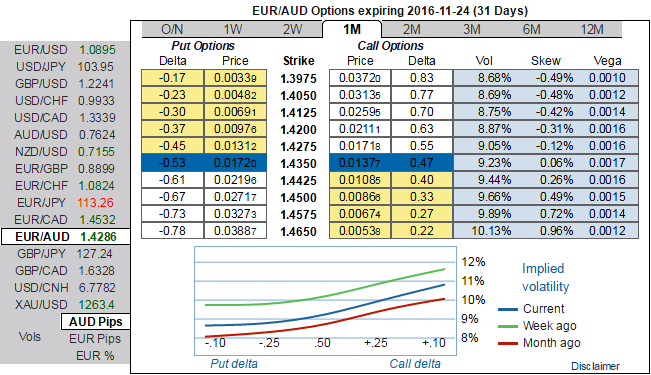

OTC outlook and option strategy:

As a resultant effect of fundamental developments as discussed above, the sentiments in OTC market for EURAUD have been fairly balanced on either side, you can probably make out 1m IV skews that signify the importance of the OTM puts which is why we are loading up more weights in options strategy that mitigates downside risks.

Volatility smiles most frequently show that traders are willing to pay higher implied volatility prices as the strike price grows aggressively out of the money.

The current spot FX is trading at 1.4285 and showing little strength from last Thursday, since major trend appears to weaker to extend slumps up to 1.4183, 1.4072 and 1.3950 levels seem quite possible events with the major barriers being 1.4425 and 1.4509 levels on the flip side, aggressive bears can initiate hedging strategy either by using longs in 1 lot of 1m ATM -0.49 delta put, 1 lot of 1m (1%) OTM -0.36 delta put and simultaneously, long in 1 lot of 2w ATM +0.51 delta call options, the strategy would be entered at net debit but reduced hedging cost as we’ve chosen OTM strikes in the strategy.