U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks

BOJ Raises Interest Rates to 31-Year High, Signals Strong Focus on Inflation Risks  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  BOJ Raises Interest Rates to 1% as Inflation Pressures Persist

BOJ Raises Interest Rates to 1% as Inflation Pressures Persist  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

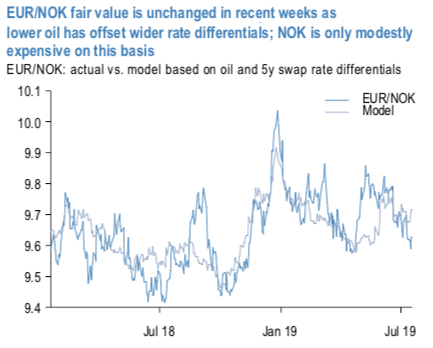

NOK’s lagging performance despite a wider rate differential is explained by crude prices. Assuming usual betas relative to oil, one could argue that EURNOK should have remained range-bound, yet the cross has drifted lower (refer 1st chart). NOK is expensive on this framework, but the magnitude is modest. On longer-term REER-based metrics, NOK is closer to fair value (refer 2nd chart).

SEK remains the cheaper currency among the two on standard frameworks, but valuations alone do not warrant longs in our view. We refer to JPM’s REER model, wherein SEK is the third currency globally and the cheapest in G10 (refer 2nd chart). SEK also continues to appear cheap adjusted for rate spreads, a relationship that has been dislocated for nearly a year now. Nonetheless, we don’t think this warrants long SEK exposure as the Riksbank is likely to be vulnerable to a dovish capitulation as the ECB becomes more dovish, and also since SEK is still among the lowest yielders globally. With the next rate RB hike at least 6 months away, there is little urgency to scale into SEK longs.

Active trade recommendations include long NOK exposure. NOK remains our preferred Scandi FX given a resolute central bank and higher yield and we retain residual exposure to this view in the trade recommendations (via a short in a 1.08 NOKSEK put with 1m left to expiry).

We also re-initiated EURNOK shorts intra-month motivated by a desire to a) increase the magnitude of EUR shorts in our portfolio on of the July 25th ECB meeting, where the balance of risks are skewed towards a more dovish direction in our view, and b) partially reduce the short high beta FX exposure in our portfolio. The risk to a tactically short EURNOK view is its sensitivity to a deterioration in risk sentiment, which is still possible given the soft global growth backdrop.

Medium-term views on both currencies are modestly bullish on gradual rate hikes, which puts them in contrast with other G10 central banks. EURSEK 1- year ahead target is unchanged at 10.45 so a 1% spot strengthening vs. the euro. EURNOK forecast 1-year ahead of the target is also unchanged at 9.60, also a 1% strengthening in spot terms (2.5% in total return terms). Risk bias for both currencies is kept unchanged at bearish given the downside tail risks to global growth and both are high beta currencies. Courtesy: JPM