Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei

BOJ Rate Hike Expected to Boost Yen, Impact USD/JPY and Nikkei  Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate

Indonesia Central Bank to Draft New Regulations After Expanded Economic Growth Mandate  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists

RBA Minutes Signal Australia Central Bank Remains Ready to Raise Interest Rates if Inflation Persists  FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022

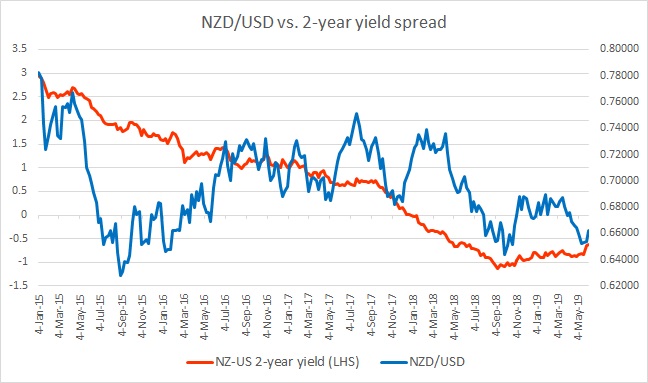

The chart above shows, how the relationship between NZD/USD and 2-year yield divergence has unfolded since 2015.

While the spread has narrowed steadily from +300 basis points (bps) in January 2015 to -106 bps as of September 2018, the New Zealand dollar has been pretty volatile around the spread. However, from the chart, it’s quite clear that the direction of the spread is playing a crucial role over the medium to long term.

We have forecasted a lower NZD against the USD with a target of 0.59 against the USD over the medium to long term, and with the Reserve Bank of New Zealand (RBNZ) continuing its dovish rhetoric, we expect the spread to decline further in favor of the USD.

As the spread started narrowing in favor of the New Zealand dollar since September, the New Zealand dollar rose against the USD. Since September, the spread has narrowed from -112 bps to -80 bps as of March, as the Kiwi is up from 0.65 area to testing the 0.69 resistance area.

However, as RBNZ reduced rates by 25 bps n April, the spread has once again widened to-84 bps and the New Zealand dollar declined to 0.658 against the USD.

In June, the spread has continued to narrow and rose to -62 bps, while NZD/USD consolidating around 0.662 area.