RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks

RBI Holds Interest Rates at 5.25%, Cuts India Growth Forecast Amid Rising Global Risks  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat

Goldman Sachs: US Dollar Likely to Stay Strong Despite Oil Price Retreat  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027

Goldman Sachs Sees Fed Holding Interest Rates Steady Until 2027  Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?

Trump’s Iran Strategy: What Has Been Achieved After Three Months of Conflict?  Today’s space race could turn fatal if we don’t agree on new rules

Today’s space race could turn fatal if we don’t agree on new rules  How AI prompting turned writerly description into an everyday skill

How AI prompting turned writerly description into an everyday skill  BOJ June Rate Hike Likely as Inflation Risks Rise Amid Middle East Tensions

BOJ June Rate Hike Likely as Inflation Risks Rise Amid Middle East Tensions  RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200

RBA Expected to Hold Interest Rates at 4.35% as Markets Watch AUD/USD and ASX 200  ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

ECB Set to Raise Interest Rates as Energy Shock Fuels Eurozone Inflation Concerns

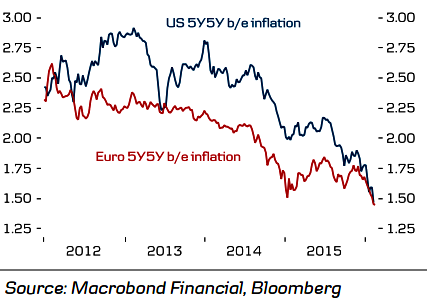

Long-term inflation expectations in both the US and the euro area have trended lower for a long time and at 1.5% are clearly below inflation targets (2% for the US and below but close to 2% for the euro area). While Fed officials have worried about inflation being too low, they have also maintained that the factors holding back inflation are transitory. Significant gains remain a challenge against the backdrop of tighter financial market conditions, recent sharp stock market sell-off and slowing domestic and global growth.

Data released last Friday showed that US overall CPI remained unchanged in Jan after slipping 0.1 percent in Dec. The CPI increased 1.4 percent in the 12 months through Jan, the biggest rise since Oct 2014, after gaining 0.7 percent in Dec. We are skeptical that the rise in core CPI would be sustained. However, revisions to the inflation data shows underlying inflation a bit firmer in the last months of 2015 than previously reported.

"This was a firm, broad-based rise in core inflation that should dispel the notion, evident in market-based measures of inflation compensation, that the economy can't generate any inflation," said Omair Sharif, rate sales strategist at SG Americas Securities in New York.

Following the strong core CPI reading, the Fed's preferred personal consumption expenditures (PCE) price index (data next Friday), excluding food and energy, is now expected to increase 0.2 percent in Jan after slipping 0.1 percent in Dec. The core PCE is forecast rising 1.6 percent in the 12 months through Jan after increasing 1.4 percent in Dec.

Global growth slowdown and turbulence in markets are further dampening hopes of economic recovery in the eurozone and this is feeding into lower inflation expectations. The minutes of the ECB's January meeting showed that growth and inflation risks were already on the rise in the euro area and some policymakers are advocating pre-emptive action in the face of new threats. The market is already pricing aggressive easing from the ECB and a Fed on hold until 2017.

EUR/USD has retraced a bit following the sharp rise recently. This is a natural response to a turn in risk appetite, as the EUR is acting as a funding currency and tends to weaken when sentiment turns more positive. Relative rates have also moved a bit in favour of the EUR compared with the USD. EUR/USD is likely to trade higher in the medium term. The major was trading at 1.1056 as of 1130 GMT.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

Lower inflation expectations could trigger central bank actions

Monday, February 22, 2016 11:50 AM UTC

Editor's Picks

- Market Data

Most Popular