FxWirePro: Daily Commodity Tracker - 21st March, 2022

FxWirePro: Daily Commodity Tracker - 21st March, 2022  Gold Prices Fall Below $4,000 as Strong Dollar, Fed Rate Hike Bets Weigh on Bullion

Gold Prices Fall Below $4,000 as Strong Dollar, Fed Rate Hike Bets Weigh on Bullion  SpaceX Eyes Starlink Mobile Phone Service to Challenge Verizon, AT&T, and T-Mobile

SpaceX Eyes Starlink Mobile Phone Service to Challenge Verizon, AT&T, and T-Mobile  Best Gold Stocks to Buy Now: AABB, GOLD, GDX

Best Gold Stocks to Buy Now: AABB, GOLD, GDX  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Trump Requests $11 Billion More in Farm Aid as Rising Costs Pressure U.S. Farmers

Trump Requests $11 Billion More in Farm Aid as Rising Costs Pressure U.S. Farmers  White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response

White House Seeks $87.6 Billion Emergency Funding for Iran War, Farmers, and Ebola Response  Wall Street Ends Mixed as Tech Stocks Struggle Ahead of Micron Earnings

Wall Street Ends Mixed as Tech Stocks Struggle Ahead of Micron Earnings  South Korea Remains MSCI Emerging Market Despite Reform Progress

South Korea Remains MSCI Emerging Market Despite Reform Progress

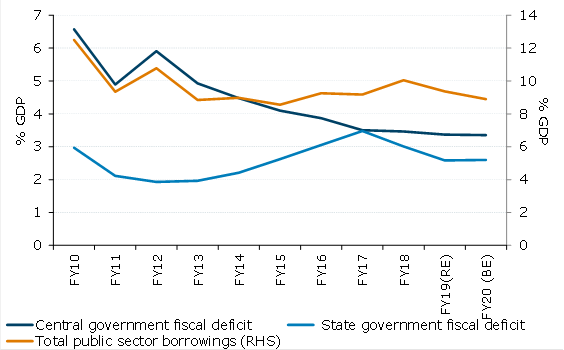

The inability of bond yields to break lower despite an unprecedented scale of liquidity infusion by the Reserve Bank of India (RBI) and expectations of further monetary easing is explained by the worsening fiscal position, according to the latest report from ANZ Research.

The government has now deviated from the fiscal roadmap in four of its five years in tenure. The medium term fiscal deficit target of 3 percent of GDP, initially to be achieved in FY17 (fiscal year ending March 2017) has been pushed out to FY21 (fiscal year ending March 2021).

Higher off-budget funding of public capital spending has also under-stated the real extent of India’s fiscal deficit. The management of the disinvestment process has also shifted from initial public offerings to the public to private placements with state-owned insurance companies and share buybacks by state enterprises, the report added.

At the current run rate, the combined central-state government debt ratio of 60 percent can be attained by the revised timeline of FY25 as laid out in the fiscal roadmap. This is however, sensitive to the underlying assumptions, especially nominal GDP growth.

"The current accommodative fiscal-monetary mix has not filtered through to the currency market as yet. The closure of the output gap, which will also result in a widening of the current account deficit, could well be the inflexion point," ANZ Research further commented.