Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges

Over the holiday season, as we stated in our earlier posts USDTRY has been creeping ever closer to the 6.00 mark (refer 2nd chart). To what extent this is the result of low liquidity and to what extent it is the future ‘trend’ will be clear soon after market participants return from holiday. We have long held the view that USDTRY would rise sharply during the next EM risk off episode – the reason for such a view is the asymmetric reaction function of the central bank, which can only cut rates but not hike them; this alone is a sufficient condition for the lira to weaken significantly in the medium-term. Because of TRY’s high carry, we need a strong initial trigger for decline. We open this week following geo-political developments involving the US and Iran, which give us little re-assurance that a risk-off scenario can be excluded in the near-term. What is more, local developments are not helpful either: latest CPI data do not bode well for the lira.

In December, headline inflation accelerated to c.12% and core inflation accelerated back to c.10%. CBT has responded to lira weakness with secondary policy tweaks: a hike to FX RRR by 200bps for banks which are not lending aggressively enough; and plans to impose an additional fee on FX RRR balances.

In late-December, CBT hiked the RRR on forex deposits and participation funds by 200bps, except for banks which are lending fast enough to meet CBT's reference range for real lira loan growth. This move aims to simultaneously incentivise lending, while building up the CB’s FX reserves. The latter policy will impose c. 0.025% fee on RRR balances, in a kind of financial service tax, which will aim to dis-incentivise dollarization of the banking system. From the point of view of the main policy objective at present, which must be to curb lira depreciation, we find these measures to be neutral – not having any effect whatsoever. We look for higher USDTRY levels in the month ahead.

Hedging Strategy:

On hedging grounds, 2m USDTRY debit call spreads are advocated with a view to arrest upside risks. Initiated 2m 5.50/6.24 call spreads at net debit. One achieve hedging objective as the deep in the money call option with a very strong delta will move in tandem with the underlying spikes.

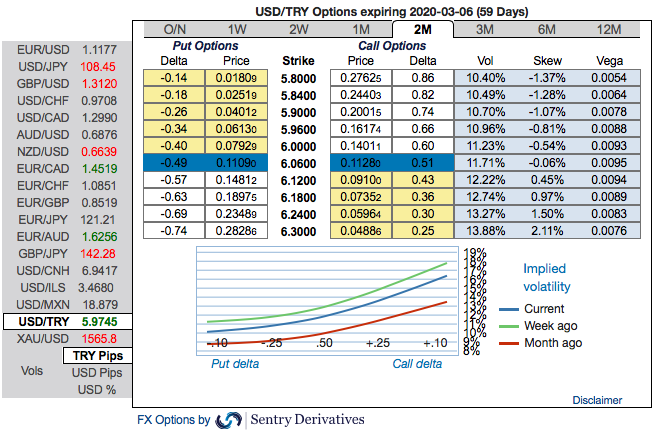

It seems that hedgers of TRY are positioned for the upside risks on the above fundamental factors. The positively skewed IVs of 2m tenors are bidding for OTM calls strikes up to 6.30 levels (refer 1st chart).

IVs of this underlying pair is also on the higher side, trending highest among the G20 FX space. Call options with a higher IVs cost more, because, increasing IV is conducive for the option holder, just for an intuition that the higher likelihood of the market ‘swinging’ in holder’s favour. Courtesy: Sentry & Commerzbank