New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks

BoE Policymaker Alan Taylor Signals No Need for Interest Rate Hike Amid Iran War Inflation Risks  AI can be a personal trainer in your pocket – but is it safe?

AI can be a personal trainer in your pocket – but is it safe?  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence

Indonesia Plans Higher Asset Yields to Boost Rupiah and Restore Investor Confidence  RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough

The government is ‘doubling down’ on its social media ban. But bigger penalties for platforms aren’t enough  Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says

Europe Heatwave Creates Growth Opportunity for Carrier, Trane, and Johnson Controls, Citi Says  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

BOJ Rate Hike Expectations Rise as Weak Yen and Strong U.S. Jobs Data Increase Pressure

The pessimistic USD outlook is based on the expectations that growth will rise globally, causing other major central banks like the ECB and the Bank of Japan to normalize their monetary policies. What supports this view is that US inflation can be used to estimate global inflation pressure.

The higher inflation in the US should, therefore, fuel price pressure globally, increasing the likelihood of a reduction in monetary policy stimulus elsewhere. The currencies of the central banks concerned should benefit from that - at the expense of USD.

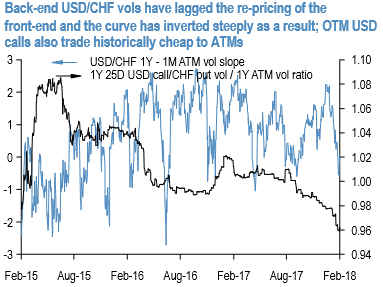

OTM USD calls/CHF puts as a vega play: While 1M CHF ATM vols have jumped 2% pts. YTD, longer expiries have lagged, leading to a fairly steep inversion of the vol curve (refer above 1st chart).

Owning 6M-1Y vega, therefore, carries no roll-down penalty while allowing patience to await a shift in SNB policy. The additional kicker is that longer expiries cover the US mid-term elections which are too far away for the market’s focus now but should gradually gain in importance with the passage of time.

A twist on ATM vega is to own OTM USD calls/CHF puts i.e. the weak / “wrong” side of the risk-reversal on a delta-hedged basis.

The near-extreme bid for USD puts on risk-reversals implies that USD calls trade at a sizeable, multi-year high discount to ATM vols (refer above 1st chart).

In addition to current value, OTM USD calls also have a track record of performing comparably with ATM vols (refer 2nd chart) without costing smile theta, which renders them attractive vehicles to not only position for an SNB rethink that proves more disruptive than markets anticipate, but also a more garden variety equity/dollar correction for which the relatively cheap USD calls are the “correct” side of the risk-reversal to own.