Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic

Jerome Powell Attends Supreme Court Hearing on Trump Effort to Fire Fed Governor, Calling It Historic  Why Trump’s new pick for Fed chair hit gold and silver markets – for good reasons

Why Trump’s new pick for Fed chair hit gold and silver markets – for good reasons  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness

Bank of Japan Signals Cautious Path Toward Further Rate Hikes Amid Yen Weakness  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

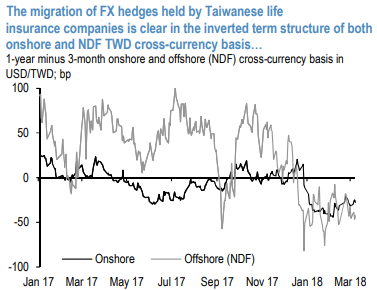

In longer dated vols, this week indicated that Taiwanese life insurance companies were actively extending the maturity of their FX hedges, Bloomberg reports.

Whereas in the past they had focused primarily on 3-month swaps—the vast majority of which are executed onshore — anecdotal evidence from the region indicated a growing preference for 1-year and potentially longer tenors.

We can see evidence of this in FX forward pricing, where the term structure of both onshore and NDF cross-currency basis recently inverted (refer 1st chart).

Though not a regime shift by any means, such a change in hedging strategy is likely intended to mitigate the potential impact of Fed hikes on FX hedging costs. It is important to note, however, that with nearly 75% of our forecast for four hikes over the next year priced into the curve, barring a significant acceleration in Fed tightening we think 1-year maturities are unlikely to offer meaningful savings over rolling shorter-dated hedges.

Further, given more limited onshore liquidity in these points, they are exposed to the noticeably higher volatility exhibited by NDFs. In the meantime, given the relative slopes of the USD and TWD swap curves, carry on hedged foreign assets is likely to deteriorate as a greater fraction of their hedge book is pushed into longer tenors (refer 2nd chart). In fact, such a shift will likely make EUR-denominated assets—which already offer better relative value— look that more attractive by comparison. Courtesy: JPM

FxWirePro launches Absolute Return Managed Program. For more details, visit: