US Dollar Climbs to One-Year High as Fed Rate Hike Expectations Surge

US Dollar Climbs to One-Year High as Fed Rate Hike Expectations Surge  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S.-Iran Diplomacy Helps Drive Gasoline Prices Down 15% From May Highs

U.S.-Iran Diplomacy Helps Drive Gasoline Prices Down 15% From May Highs  South Korea’s KOSPI Rebounds as Samsung and SK Hynix Lead Tech Stock Recovery

South Korea’s KOSPI Rebounds as Samsung and SK Hynix Lead Tech Stock Recovery  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  US Stock Futures Recover as Iran Signals Progress in Peace Talks

US Stock Futures Recover as Iran Signals Progress in Peace Talks  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Japan Keeps Markets Guessing as Yen Nears 40-Year Low, Raising Intervention Risks

Japan Keeps Markets Guessing as Yen Nears 40-Year Low, Raising Intervention Risks  South Korea Stocks Tumble as AI-Fueled Rally Faces Profit-Taking Pressure

South Korea Stocks Tumble as AI-Fueled Rally Faces Profit-Taking Pressure  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

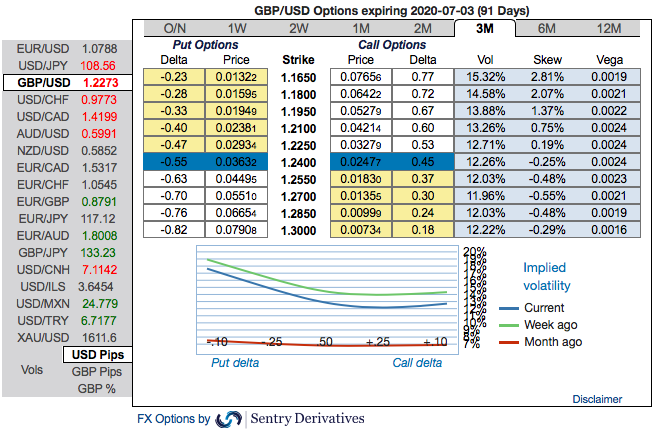

GBP’s performance ranks mid-table over the past month (+0.5% vs USD, -2.5% vs EUR) as the global impact of the coronavirus has come to dominate GBP's local difficulties with Brexit. But even though Brexit is now being overshadowed by an even more existential crisis, this doesn’t let GBP off the hook, far from it actually, as the accelerated removal of GBP's interest rate support as the BoE prepares to respond to the COVID-19 shock will further undermine the sustainability of the UK's worst-in-class current account deficit (a 4-5% of GDP current account gap is incompatible with the UK's new reality as a low-growth, low-yielder).

In addition, while Brexit is being overshadowed, this is only temporary and GBP remains vulnerable from a great sense of realism amongst investors about the government's objectives for the EU trade talks and its credible threat still to walk away in the pursuit of regulatory autonomy from the EU and freedom from strict level playing field commitments.

As a result of the Brexit-virus one-two we are lowering the GBP forecast. The point of maximum jeopardy is expected to be around mid-year as the trade talks reach their make-or-break point (remember that the government has legally barred the transition period from being extended beyond end-2020) and the risk of no- deal crescendos.

Options Strategy (Debit Put Spread): Contemplating above factors, wise to deploy diagonal options strategy by adding short sterling: Stay short a 1M/2W GBPUSD put spread (1.25/1.14), spot reference: 1.2340 level.

The Rationale: Observe the 3m GBP’s positive skewness that has stretched towards OTM Put strikes, hedgers have shown interests for bearish risks.

To substantiate the downside risk sentiment, risk reversal numbers have still been signalling bearish hedging sentiments in the long run. Hence, we advocate the diagonal options strategy on both hedging and trading grounds.

Alternatively, activate shorts in GBPUSD futures contracts of April’20 deliveries with an objective of arresting potential slumps. Courtesy: Sentry, JPM & Saxo