China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis

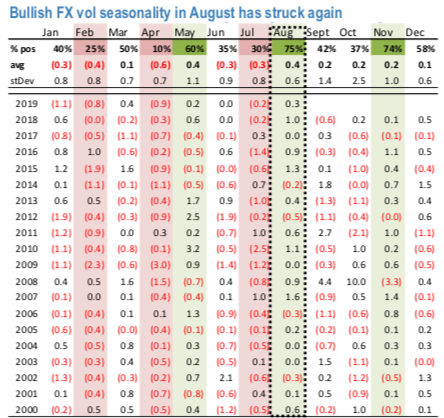

The brutal late-summer bullish seasonality of FX vol (refer 1stchart) has re-asserted itself following an eventful FOMC meeting and a rather more dramatic turn of events on US/China trade towards the fag end of the week. Before being overshadowed by the Presidential tweets that upended any lingering hopes of quiet late summer markets, the “hawkish” Fed cut at the July FOMC could reasonably have been expected to be the marquee event catalyst of the week likely to produce durable market impact over the next few weeks.

A consensus had begun to emerge around soft US exceptionalism and contained dollar strength in the lead-up to the September ECB, as uber-dovish Fed expectations were revised to reflect a more reasonable assessment of concurrent US activity data, and the old strong-US-weak- Europe cyclical/policy divergence narrative revived.

The latest tariff threat from Trump emphatically reinforces this notion of dollar bullishness; the crucial difference for FX volatility is the potential for greater velocity and urgency to dollar rallies than might have been previously anticipated. The net result is a sharp re-pricing higher of front-end implied vols across the board, with the largest increases focused on Asian currencies in the eye of the storm and China-linked high-beta EMs such as ZAR (refer 2ndchart).

In light of the further escalation in the US-China trade conflict, we are revising our USDCNY forecast profile higher. As we have noted in recent research (see China FX focus: Life after 7.00) the risks around a break of 7.00 have arguably never been greater. With tariffs likely to be applied to the remaining set of Chinese exports to the US, upside pressure on USDCNY should only increase, as a weaker currency should be part of the first-order response to such a loss of competitiveness. This has been evident in 2018 and in May of this year after the US raised tariff rates on Chinese exports. Courtesy: JPM