2025 Market Outlook: Key January Events to Watch

2025 Market Outlook: Key January Events to Watch  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision

Indian Government Bonds Seen Opening Steady Ahead of RBI Policy Decision  BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures

BOJ Signals More Rate Hikes as Inflation Risks Rise Amid Energy Price Pressures  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

The Bank of Japan (BoJ) got its Christmas presents firstly on 8th November and now again on 14th December: since the US Presidential elections the yen has been under pressure against USD. Thanks to Trump. As a result, the BoJ can be a little more relaxed when facing the next round of ugly inflation data tomorrow.

It will stick to the control of the yield curve for the foreseeable future, which means getting the Fed to do its work for it. Does that make it any more likely that it will reach its inflation target? Hardly, but at least it eases the pressure on the BoJ.

In yesterday’s Fed’s meeting (14th Dec), as broadly anticipated, the FOMC was upbeat and more hawkish than anticipated. Yes, the FOMC raises the target range of the fed funds rate by 25bps − the first rate hike since December 2015.

Most importantly, after a prolonged duration of downgrades to the dot plot, the FOMC modestly tweaked up the profile. Three 25bps hikes are now expected in 2017, up from two.

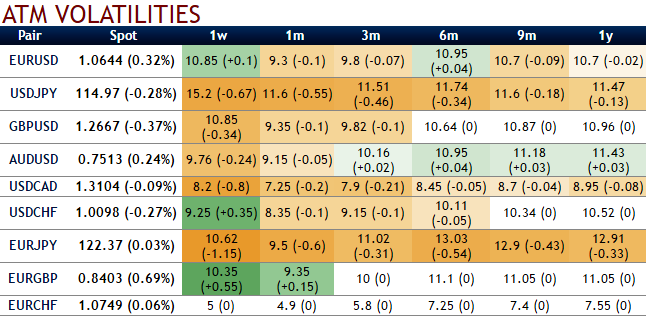

OTC outlook:

Yen vols were a marked outperformer this year as USDJPY shed nearly 17% peak-to-trough, but this is likely to change going forward under the aegis of the BoJ’s yield curve control framework that has worked to anchor JGB yields better than we expected, and as the pair encounters offsetting forces of higher US-Japan rate differentials and greater risk-aversion from EM weakness.

USDJPY risk-reversals: As a result of the above fundamental developments, the hedgers of USDJPY began bidding OTM call strikes as you could see positive changes in risk-reversals. But these numbers in longer tenors are still very much a work in progress as far as vol selling opportunities go, with current levels (3M risk reversals at shy above 11.5 vols & with increased pace in 6m vols for USD puts over USD calls) still removed from post-Brexit extremes (2.8), while 3m IV skews to substantiate bearish hedging offered by risk reversals. But short-term risks reversal bets signals the higher potential of USD.

Needless to say, selling expensive yen calls should prove profitable amid such a mild updraft in USDJPY spot.

Hence, contemplating above risk reversal adjustments, we foresee the opportunities in writing overpriced ITM puts coupled with adding long positions in ATM delta puts long-term tenors.

From positive risk reversal flashes you can probably figure out hedging operations for upside risks in both in short run and long run are intensive, while 1m IV skews also signify the hedging interests in OTM call strikes.