Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand

Lithium Market Poised for Recovery Amid Supply Cuts and Rising Demand  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Urban studies: Doing research when every city is different

Urban studies: Doing research when every city is different  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  Mexico's Undervalued Equity Market Offers Long-Term Investment Potential

Mexico's Undervalued Equity Market Offers Long-Term Investment Potential  Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios

Fed May Resume Rate Hikes: BofA Analysts Outline Key Scenarios  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Gold Prices Fall Amid Rate Jitters; Copper Steady as China Stimulus Eyed

Japanese Manufacturing:

The latest survey data signalled a slight improvement in operating conditions at Japanese manufacturers. Production rose for the second consecutive month, while total new orders declined at the weakest rate in the current eight-month sequence of contraction. International demand also increased for the first time since the start of 2016.

Most notably, the new exports orders rise for the first time in eight months.

It is derived from indicators for new orders, output, employment, suppliers’ delivery times and stocks of purchases. Any figure greater than 50.0 indicates the overall improvement of sector operating conditions. The headline PMI posted at 50.4 in September, up from 49.5 in August and signalling a modest improvement in manufacturing conditions. Moreover, the latest reading was the highest since January and broadly in line with the long-run average (50.6).

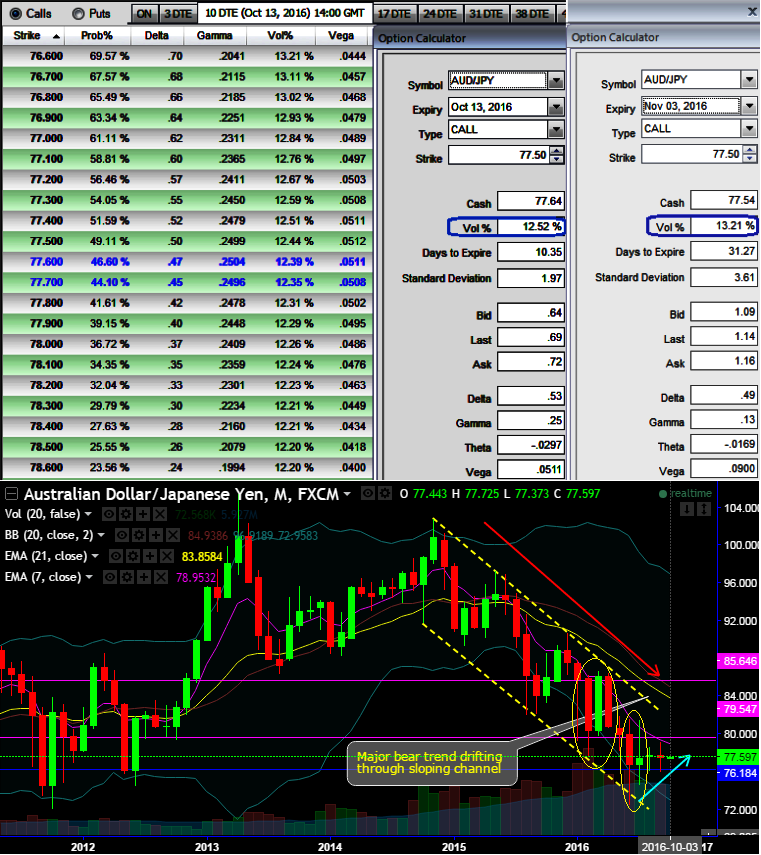

OTC outlook and hedging framework:

We believe ongoing AUDJPY upswings move in sync with 1w ATM IVs - rallies and HY vols likely to favour PRBS.

This pair has been oscillating between 76.739 and 76.065 levels, showing mild upswings but long term declining trend seems to be intact as you can see the convincing volumes and technical indicators favouring bears on the monthly charts.

ATM IVs of AUDJPY is rising a shy above 12.5% as shown in the diagram the standard deviation these call option is flashing up at 1.97. While IVs of ATM contracts of 1m tenors are spiking crazily at 13.21%, this has been justified by historical volatilities in spot FX fluctuations (see big real body candles on monthly technical charts).

Traders tend to view the put ratio back spread as a bear strategy because it employs puts. However, it is actually a volatility strategy. The implied volatility of 1M ATM put contract is at 16% and it is quite higher side when long-term trend is bearish and spikes in previous rallies for short term which is a good sign for option writers.

Since the spot Fx of the underlying pair is rising along with IVs from last couple days, this is good news for option writers as such options with a higher IV costs more. Thereby, writers are likely to receive more premiums.

Well, on the contrary, if the same IV during longer tenors keep increasing and you are holding an option, this is good for holders as well. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

As we expect the underlying currency exchange rate of AUDJPY to make a larger move on the downside. As shown in the figure purchase 1M 1 lot of at the money -0.51 delta put, 2M 1 lot of (1%) out of the money -0.35 delta put and sell 2W one lot of (1%) In-The-Money put option using prevailing rallies.