US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Global Markets React to Strong U.S. Jobs Data and Rising Yields

Global Markets React to Strong U.S. Jobs Data and Rising Yields  With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?

With Iran and the US signing a peace deal, where does that leave Benjamin Netanyahu?  Geopolitical Shocks That Could Reshape Financial Markets in 2025

Geopolitical Shocks That Could Reshape Financial Markets in 2025  U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?

U.S. Stocks vs. Bonds: Are Diverging Valuations Signaling a Shift?  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data

Aussie retail sales prints again disappointed, with sales in June rising by just 0.1% MoM despite a bounce-back in clothing sales. Retail sales fell in both NSW and Victoria. Interestingly, the weakness is concentrated in sales by small retailers. In real terms, retail sales rose by 0.4% in Q2 while retail price inflation remained muted.

But GBPAUD doesn't seem to have discounted, the pair has been stagnantly trading at 1.7496 levels awaiting for BOE rate decision.

Today’s data highlight some underlying fragility in the economy and reinforce the appropriateness of ultra-easy monetary policy settings. On the contrary, the trade balance in U.K. has expanded from previous -9.9B to the current -10.3B in line with the forecasts.

The FX market has priced that in and any extreme or dramatic weakness in GBP as a result of today’s cut is unlikely but bears are likely to drag further is a certain event.

Instead what will be decisive for the GBP exchange rates will be whether the BoE implements further measures. Some BoE officials had already signalled that they would support further measures. It is therefore hardly surprising that approx. half of analysts polled by Bloomberg expect the bond purchasing programme to be re-activated today.

With resultant effects, the GBPAUD cross is anticipated to depreciate further, most likely towards 1.7025 levels.

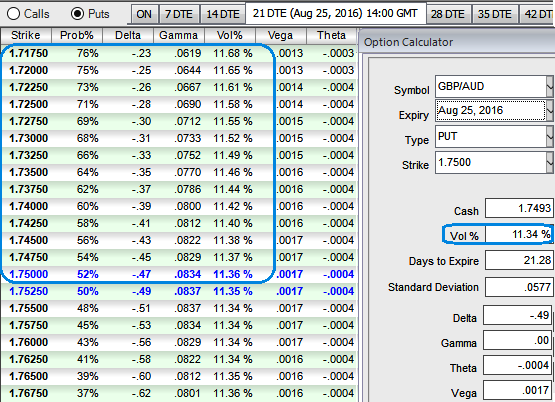

BoE's rate decision would be released which is likely to add pressures on sterling but the potential risks of post-Brexit event keeps adding more pressures, in addition to this refer above diagram for IVs and sensitivity marks in FX options due to the U.K's interest rate speculations, OTM put strikes are on competitive advantage.

Historically, the pair has been very well reacting as per earlier analysis and we maintain our next bearish targets at 1.7025 levels.

Since OTC markets seem to be highly volatile with an extremely bearish environment, and IVs for 1M contracts are expected to fade away (at around 11% and above). This would be a good news for option holders contemplating the prevailing bearish environment but more number of longs in ATM delta puts would ensure the reasonable probabilities in underlying exposures.

To factor in the weakness in this pair as we could see reasonable IVs even in next 1-3m expiries, we recommend capitalizing more on bearish signals and the IV factor in the long term by employing OTM longs matching with ATM longs to construct back spreads that likely to fetch positive cash flows.

So, here goes the strategy this way, Go long in 2 lots 1M ATM -0.50 delta puts, long in 2M (1%) OTM -0.35 delta put, and simultaneously short 2W (1%) ITM shorts, the spread is to be executed in the ratio of 3:1with net delta at around -0.70.