RBI Hits Pause as Geopolitical Storm Clouds Gather

RBI Hits Pause as Geopolitical Storm Clouds Gather  South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated

South Korea Signals Possible Interest Rate Hike as Inflation Remains Elevated  Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data

Oil Prices Dip Slightly Amid Focus on Russian Sanctions and U.S. Inflation Data  Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?

Should I take zinc or eat oysters to ward off colds, boost my immune system or improve fertility?  Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey

Central Banks Eye Gold, Reduce Dollar Exposure as AI Adoption Accelerates: OMFIF Survey  Elon Musk is remaking the world, like Henry Ford before him – but more dangerously

Elon Musk is remaking the world, like Henry Ford before him – but more dangerously  Wall Street Analysts Weigh in on Latest NFP Data

Wall Street Analysts Weigh in on Latest NFP Data  Stock Futures Dip as Investors Await Key Payrolls Data

Stock Futures Dip as Investors Await Key Payrolls Data  Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand

Michael Burry Shorts Tesla at $416 as AI and Semiconductor Bearish Bets Expand  U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures

U.S. Treasury Yields Expected to Decline Amid Cooling Economic Pressures  In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land

In a rebuke to Trump, the Supreme Court rules that birthright citizenship is the law of the land  A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.

A Korean Family Spent 34 Years Hoarding Chinese Tea. Now They're Putting It on the Blockchain.  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

China Sets 1.25% Overnight Reverse Repo Rate Below Market Expectations

The drivers of the dollar’s expected medium-term grind weaker in the refreshed forecasts are largely the same ones as we originally outlined in our recent post although the trade-weighted dollar Index has gone up by 0.2% and is up 1.7% since mid-Feb. The late-cycle growth and rate hikes in the US economy providing diminished support for the dollar, against early-cycle policy normalization in most of the rest of G10, and stronger synchronized global growth supporting the high-beta blocs of EM and commodity FX.

More and earlier dollar weakness in our forecast revisions simply reflects these forces coming into play sooner and more forcefully than originally expected, given various upgrades to global growth and policy normalization expectations that our economics colleagues have introduced to-date.

Nevertheless, it is notable that further dollar weakness is expected in spite of another material upgrade to US growth forecasts, following a likely second round of fiscal stimulus being delivered by Washington budget negotiations.

It rallied on the back of the Fed’s lead in the monetary policy cycle. Not only is the rest of the world slowly catching up, but it seems increasingly clear that the Fed will remain extraordinarily cautious in its policy moves. We expect the Fed Funds target to peak at 2.00-2.25%, which is consistent with real 10y yields peaking not far from current levels (52bp) and well below the 72bp we saw in December 2016. That’s not negative for the dollar but means that the currency is vulnerable both to its high valuation and to improving FX fundamentals of other major currencies, including but not limited to the euro.

EM currencies rely more on carry for returns. But valuations aren’t yet demanding and the growth backdrop offsets gradual Fed rate hikes.

While President Trump signed the proclamation on adjusting import tariffs by 25% on steel imports and 10% tariffs on aluminum imports on Thursday 8 March. Mexico and Canada have been exempted indefinitely for now, but conditional on a new NAFTA agreement. The proclamation also includes a potential for US entities to apply for an exemption. We think this could include the US oil and gas industry.

Judged by a limited historical sample, bilateral trade conflicts have tended to strengthen alternative reserve assets such as the euro, yen, and gold against the dollar.

They also tend to be growth negative for emerging markets that thrive on global trade, especially if retaliatory tariffs are involved. Despite these risks, high beta currencies have so far shown impressive resilience as investors have been reluctant to turn overly bearish given above-trend global growth. The lack of many reactions from the likes of AUD, NZD, and CAD opens up opportunities to buy under-priced option hedges.

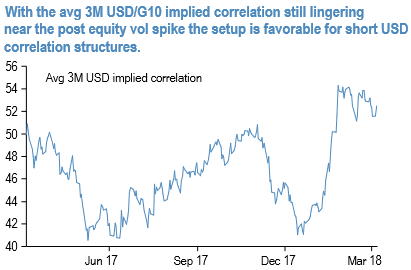

Most notably, aggregate USD-denominated implied correlations still trade near their highs from around the VIX shock (refer above chart) – a set-up that is favorable for betting on the divergence between reserve and high beta currencies via short USD correlation structures. In the recent past, we already initiated a tilt towards correlation selling via triangles of short USDJPY and NZDUSD puts hedged with long NZDJPY puts.

Currency Strength Index: FxWirePro's hourly USD spot index was at shy above 6 (which is neutral) while articulating (at 09:32 GMT).

For more details on the index, please refer below weblink:

http://www.fxwirepro.com/currencyindex

FxWirePro launches Absolute Return Managed Program. For more details, visit: