Energy Sector Outlook 2025: AI's Role and Market Dynamics

Energy Sector Outlook 2025: AI's Role and Market Dynamics  UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty

UBS Projects Mixed Market Outlook for 2025 Amid Trump Policy Uncertainty  Moldova Criticizes Russia Amid Transdniestria Energy Crisis

Moldova Criticizes Russia Amid Transdniestria Energy Crisis  UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data

UBS Predicts Potential Fed Rate Cut Amid Strong US Economic Data  S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays

S&P 500 Relies on Tech for Growth in Q4 2024, Says Barclays  US Gas Market Poised for Supercycle: Bernstein Analysts

US Gas Market Poised for Supercycle: Bernstein Analysts  U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge

U.S. Banks Report Strong Q4 Profits Amid Investment Banking Surge  European Stocks Rally on Chinese Growth and Mining Merger Speculation

European Stocks Rally on Chinese Growth and Mining Merger Speculation  China's Refining Industry Faces Major Shakeup Amid Challenges

China's Refining Industry Faces Major Shakeup Amid Challenges  Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close

Goldman Predicts 50% Odds of 10% U.S. Tariff on Copper by Q1 Close  Trump’s "Shock and Awe" Agenda: Executive Orders from Day One

Trump’s "Shock and Awe" Agenda: Executive Orders from Day One  China’s Growth Faces Structural Challenges Amid Doubts Over Data

China’s Growth Faces Structural Challenges Amid Doubts Over Data  US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts

US Futures Rise as Investors Eye Earnings, Inflation Data, and Wildfire Impacts  Bank of America Posts Strong Q4 2024 Results, Shares Rise

Bank of America Posts Strong Q4 2024 Results, Shares Rise  Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms

Moody's Upgrades Argentina's Credit Rating Amid Economic Reforms  Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes

Gold Prices Slide as Rate Cut Prospects Diminish; Copper Gains on China Stimulus Hopes  Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Indonesia Surprises Markets with Interest Rate Cut Amid Currency Pressure

Bearish GBPAUD scenarios:

1) A no-deal Brexit (GBP down between 10% and 20%).

2) The Tories maintain opinion poll bounce under Johnson.

3) UK recession.

4) China eases policy more forcefully and commodities rally on the back of future infrastructure spend;

5) The Australian government commits to large fiscal easing, shoring up growth prospects and reducing the need for a further 50bp of easing from the RBA.

Bullish GBPAUD scenarios:

1) Tories drop in the polls, Johnson loses a no-confidence vote and the subsequent general election.

2) Article 50 is eventually withdrawn.

3) The RBA cuts rates more quickly than we expect;

4) The trade conflict between the US and China broadens;

5) The global economy slows more than expected, risking recession into year end.

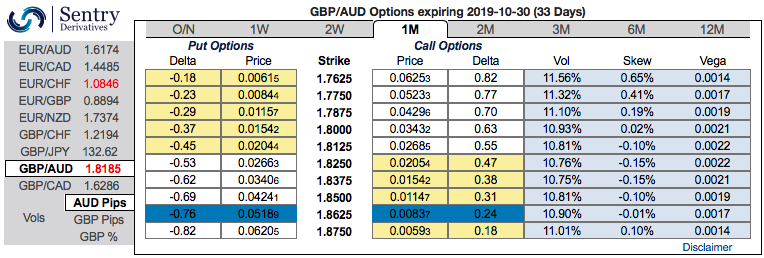

From the last 9-months or so, GBPAUD has been spiking from the lows of 1.7208 to the current 1.8186 level amid mild downswings in between. Technically, we could foresee minor price dips in the short-run and major uptrend likely to prolong further.

Hedging Framework:

3-Way Diagonal Options Spread

Ratio: (Long 1: Long 1: Short 1)

The execution: Initiate long in GBPAUD 6m at the money delta call, long 1M at the money delta put and simultaneously, Short theta in 1m (1.5%) out of the money call with positive theta or closer to zero.

Rationale: Contemplating 1Y IV skews that are well balanced on either side (positively skews on both OTM calls and OTM puts), we reckon that the Delta instruments are conducive to monitor directional risk so as to be aware that how much of option’s value would increase or diminish as the underlying market moves as this option tool measures the value of an option as the underlying spot FX moves. Well, a higher (absolute) Delta value is desirable on long leg in the above stated strategy. Whereas, the Theta is positive on short leg; as the time decay is good for an option writer (that’s why we’ve chosen narrowed expiry).

We reiterate, in the prevailing puzzled environment you could observe that the momentary bulls of GBPAUD has currently been trading in non-directionally but with some bearish pressures. Hence, we advocate the above hedging strategy with cost-effectiveness that could hedge regardless of the swings on either side.

Alternatively, on hedging grounds, at spot reference: 1.8186 levels, contemplating above technical rationale, we advocate initiating shorts in GBPAUD futures contracts of October’19 delivery as further downside risks are foreseen in the short-run and simultaneously, longs in futures of December’19 delivery.

Thereby, the foreign traders, who are dubious about puzzling swings, can directionally position in their FX exposures. The directional implementation of the same trading theme by further allow for a correlation-induced discount in the options trading also if you choose strikes appropriately. Courtesy: JPM & Sentry