FxWirePro: USD/CNY dips as China’s yuan strengthens on Iran war de escalation hopes

FxWirePro: USD/CNY dips as China’s yuan strengthens on Iran war de escalation hopes  FxWirePro: USD/JPY neutral in the near-term, scope for downward resumption

FxWirePro: USD/JPY neutral in the near-term, scope for downward resumption  FxWirePro: AUD/USD gains some ground but remains sensitive to Middle East tensions

FxWirePro: AUD/USD gains some ground but remains sensitive to Middle East tensions  FxWirePro- Major European Indices

FxWirePro- Major European Indices  FxWirePro- Woodies Pivot(Major)

FxWirePro- Woodies Pivot(Major)  FxWirePro: GBP/AUD runs out of steam but maintains bullish outlook

FxWirePro: GBP/AUD runs out of steam but maintains bullish outlook  AUDJPY Pullback Intensifies: Resistance at 110.00 Signals Short Opportunity

AUDJPY Pullback Intensifies: Resistance at 110.00 Signals Short Opportunity  FxWirePro: EUR/ NZD loses momentum but outlook is bullish

FxWirePro: EUR/ NZD loses momentum but outlook is bullish  Sterling’s Six-Week Streak Snaps: GBPJPY Slumps Toward 210.00 as Bearish Momentum Intensifies

Sterling’s Six-Week Streak Snaps: GBPJPY Slumps Toward 210.00 as Bearish Momentum Intensifies  FxWirePro: NZD/USD cautiously bid as traders sense end to Iran war

FxWirePro: NZD/USD cautiously bid as traders sense end to Iran war  Bitcoin on Edge: Geopolitical Tensions Weigh on BTC as Bulls Eye the USD 64,000 "Buy the Dip" Zone

Bitcoin on Edge: Geopolitical Tensions Weigh on BTC as Bulls Eye the USD 64,000 "Buy the Dip" Zone  FxWirePro: GBP/USD gains some upside momentum but still bearish

FxWirePro: GBP/USD gains some upside momentum but still bearish  FxWirePro- Major Pair levels and bias summary

FxWirePro- Major Pair levels and bias summary  Yen Resurgence Drives GBPJPY to 2.5-Week Low: Sellers Aim for 208.00

Yen Resurgence Drives GBPJPY to 2.5-Week Low: Sellers Aim for 208.00

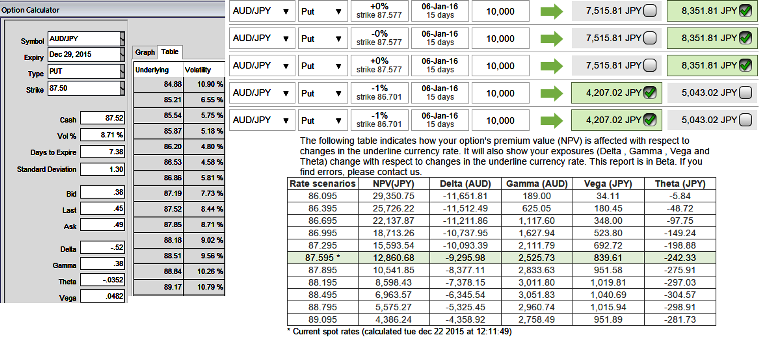

The implied volatility of 1W ATM AUDJPY put contract has nothing much changed, it is almost close to 8.71% which is quite on higher side that is good sign for option writers.

We know that the options with a higher IV cost more, intuitively due to the higher likelihood of the market 'swinging' in your favour. If IV increases and you are holding an option, this is good. You should also note short-dated options are less sensitive to IV, while long-dated are more sensitive.

As we expect the underlying currency exchange rate of AUDJPY to make a larger move on the downside in medium run. As shown in the figure purchase 2W 3 lots of At-The-Money -0.52 delta puts, and simultaneously short 3D 2 lots of (1%) In-The-Money put option.

So far we all know that the position uses long and short puts in the ratio of 2:1, now alter it into 3:2 so as to maximize the returns as we could sense the more downside potential but again it depends upon risk appetite and returns expectations.

Hence, as shown in the diagram weights have been doubled on short side and resulted into huge cash inflows for every small change in underlying exchange rate.

Entering into this AUDJPY position which has higher implied volatility at 8.71% and expecting for the inevitable adjustment is a smart approach, regardless of the direction of price movement.

Based on volatility and time decay, the strategy is a "price neutral" approach to options, and one that makes a lot of sense.

- News

- Economy

- Central Banks

- Investing

- Research

- Roundups

- Digital Currency

- Insights

- Technical Analysis

- Technology

- Business

- Law

- Health

- Nature

- Fintech

- Science

- Topic

- Opinions

- ©Econometrics LLC . All Rights Reserved.

FxWirePro: AUD/JPY hedging perspectives, good time for put writers

Tuesday, December 22, 2015 6:48 AM UTC

Editor's Picks

- Market Data

Most Popular