Oil Prices Steady as U.S.-Iran Talks Ease Supply Fears Ahead of Holiday Weekend

Oil Prices Steady as U.S.-Iran Talks Ease Supply Fears Ahead of Holiday Weekend  New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election

New Zealand Unemployment and Inflation Debate Intensifies Ahead of 2026 Election  Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears

Gold Price Today: Bullion Heads for First Weekly Gain as Weak U.S. Jobs Data Eases Rate Hike Fears  Denmark Central Bank Intervenes to Support Krone Peg Against Euro

Denmark Central Bank Intervenes to Support Krone Peg Against Euro  Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt

Supreme Court Backs Lisa Cook, Defends Federal Reserve Independence Against Trump Firing Attempt  Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations

Gold Price Surges Above $4,120 as Weak US Jobs Data Lowers Fed Rate Hike Expectations  Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets

Fed Chair Kevin Warsh Signals Policy Overhaul as Hawkish Rate Outlook Rattles Markets  U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk

U.S. Dollar Drops as Weak Jobs Data Boosts Fed Pause Bets, Yen Jumps on Intervention Talk  Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens

Turkey Vehicle Sales Fall 11.4% in June as Auto Market Weakens  US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

US Jobs Report Preview: June Payroll Growth Seen Slowing as Fed Rate Decision Looms

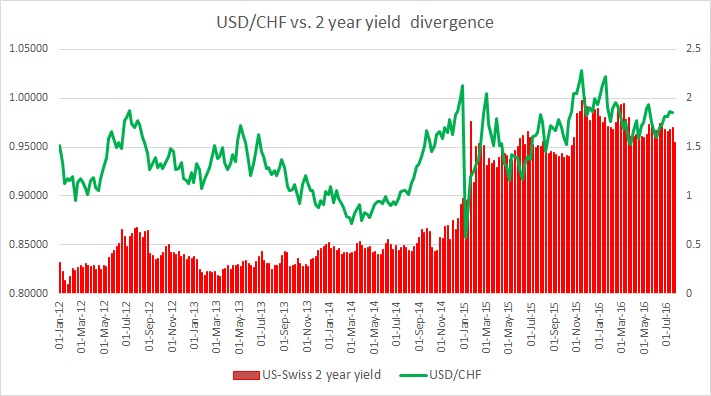

In recent days, Swiss franc’s correlation with the 2-year yield spread (US-Swiss 2 year) has dropped to 25 percent but time on time again it shows relatively high positive correlation, as high as 80 percent at times. Just before and after the Brexit referendum in the UK, the 20-day rolling correlation was averaging above 60. Hence, it is vital to keep a watch on the Swiss yields.

Just after the Swiss floor shock in January 2015 when the Swiss National Bank (SNB) removed a floor in EUR/CHF at 1.20 this relation went to negative and stayed there until October with occasional bounces to positive territory. It hasn’t gone to the negative since and was closely related to the yield (above 80 percent) in January this year.

Unlike the euro or the pound, the Swiss franc is considered a safe haven, hence the yield relation sometimes gets overlooked.

However, Swiss yields are a must watch as they are the lowest for any government bonds in the world and any shift in that will mark a major turnaround in trend. The above chart explains how the relation between the spread and exchange rate has unfolded since 2012.