Gold Falls Below $4,000 as Strong Dollar and Fed Rate Hike Expectations Weigh on Prices

Gold Falls Below $4,000 as Strong Dollar and Fed Rate Hike Expectations Weigh on Prices  South Korea’s KOSPI Plunges as Apple Price Hikes and OpenAI IPO Delay Shake AI Chip Stocks

South Korea’s KOSPI Plunges as Apple Price Hikes and OpenAI IPO Delay Shake AI Chip Stocks  Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows

Malaysia Central Bank Moves to Support Ringgit Amid Foreign Fund Outflows  Iran Attack in Strait of Hormuz Pushes Oil Prices Higher

Iran Attack in Strait of Hormuz Pushes Oil Prices Higher  Bessent Says U.S. Must Strengthen Supply Chains and Economic Security

Bessent Says U.S. Must Strengthen Supply Chains and Economic Security  Australian Household Spending Rebounds Strongly in May as Travel and Dining Drive Consumer Growth

Australian Household Spending Rebounds Strongly in May as Travel and Dining Drive Consumer Growth  Oil Prices Drop as Middle East Supply Recovery Eases Market Concerns

Oil Prices Drop as Middle East Supply Recovery Eases Market Concerns  Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman

Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman

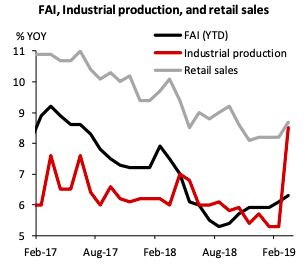

China’s gross domestic product (GDP) is expected to further witness a solid outcome in the second quarter of this year, which should offer further crucial support to the global growth picture, according to the latest report from DBS Group Research.

Looking forward, continued recovery is further expected in industrial activities and infrastructure investment. According to Premier Li’s work report, RMB800 billion and RMB1.8 trillion will be invested in railway construction and road construction & waterway projects respectively this year.

Other investments include intercity transportation, utilities, civil & general aviation as well as next generation information infrastructure. Officials have approved a large number of projects since December 2018.

And issuance of local government (LG) bond intended to fund infrastructure spending soared in Q1’19 to RMB1.4 trillion, up significantly from RMB0.2 trillion in Q1’18. Front-loading of debt allocation alleviates fiscal stress faced by local government.

Local land sales, a primary source of LG funding, have come under pressure this year as the property market cools off. A VAT cut of up to Rmb2 trillion also depresses local tax revenues.

The PMI’s employment component of the nonmanufacturing sector – where the bulk of the workforce is employed – remained in the contractionary zone for seven consecutive months. Its manufacturing counterpart also hovered near the lowest level in 7 years.

Weak labour market and tepid income growth have dampened consumer sentiment. According to the PBoC’s Urban Depositor Survey, the proportion of respondents who intended to “save more” has, over a quarter, increased by 0.9ppt to 45 percent in Q1’19. Households were also less optimistic on the outlook for property prices.

Home-related expenditure from furniture to electric & video appliances may remain lacklustre. Nonetheless, the recent increase in personal income tax threshold and expansion in deductibles is expected to lift households’ income by about 3 percent. Consumer confidence should also get a lift from the buoyant stock markets, the report further noted.

Exports jumped to five-month high last month, though the scale of the rebound was partly due to the different timing of Lunar New Year and hefty price increases. Specifically, export prices rose 4.4 percent in Q1, contributing 66.3 percent of export growth.

Emerging evidence of stimulus efficacy suggests that consumer expectation and investor confidence remain constructive. Consumption, in particular, is amenable to responding to well-targeted measures, as seen in the recent rebound in loans and retail sales figures.

This is a major source of comfort for China’s outlook as growth trends lower. Meanwhile, if growth deceleration becomes disorderly, the authorities will have the confidence that they have sufficient tools in their arsenal to stabilise the economy without having to sacrifice corporate deleveraging and associated moral hazard issue, DBS Research added in its report.

Image Courtesy: DBS Group Research