S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges

S&P Affirms Brazil’s BB Credit Rating with Stable Outlook Amid Fiscal Challenges  Wall Street Ends Mixed as Micron Surges, Apple Drops After Price Hikes

Wall Street Ends Mixed as Micron Surges, Apple Drops After Price Hikes  Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies

Japan Signals Preference for Low Interest Rates as BOJ Policy Debate Intensifies  Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman

Oil Prices Rebound as Strait of Hormuz Tensions Return After Ship Attack Near Oman  US Dollar Slips After PCE Inflation Data Eases Fed Rate Hike Expectations

US Dollar Slips After PCE Inflation Data Eases Fed Rate Hike Expectations  Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand

Gold Prices Rise Above $4,000 as Inflation Data and Weaker Dollar Boost Demand  U.S. Dollar Reaches One-Year High as Tech Sell-Off and Fed Rate Hike Expectations Support Demand

U.S. Dollar Reaches One-Year High as Tech Sell-Off and Fed Rate Hike Expectations Support Demand  BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks

BOJ Hawk Signals Faster Interest Rate Hikes Amid Inflation Risks  Asian Currencies Trade Mixed as Yen Hovers Near 40-Year Low, Dollar Holds Firm on Fed Outlook

Asian Currencies Trade Mixed as Yen Hovers Near 40-Year Low, Dollar Holds Firm on Fed Outlook  Oil Prices Drop as Strait of Hormuz Shipping Recovers

Oil Prices Drop as Strait of Hormuz Shipping Recovers

International developments moved to the back seat this week, as the risks stemming from Greek debt crisis and China’s equity market eased off for now. However, renewed weakness in commodity sector and concerns over corporate profitability weighed on market sentiment.

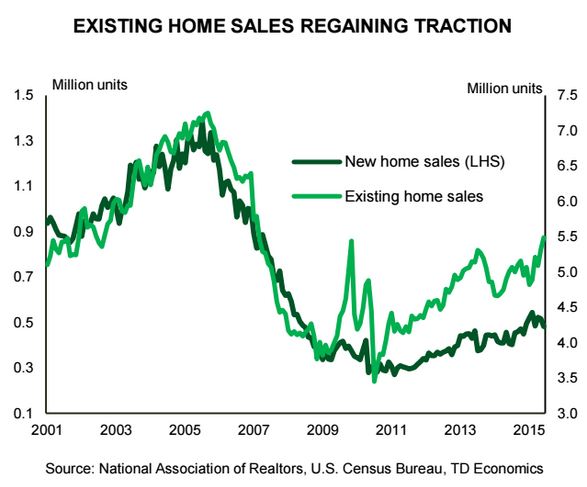

The domestic data flow remained relatively upbeat. Initial jobless claims fell to a multi-decade low. Existing home sales rose by 3.2% in June to a new cycle high. New home sales disappointed, declining by 6.8% in June, however they were still up 18% relative to a year ago.

Next week should bring further evidence of a rebounding economy, with second quarter GDP reading expected to show a 2.5% gain. The upturn in economic data is likely to be recognized in the Fed’s July interest rate announcement, which we expect to set the stage for September rate liftoff.